Introduction

The first quarter of 2025 was interesting to say the least. In January, President Trump was sworn into office and immediately got to work. He nominated his entire cabinet and signed 89 executive orders, several of which touch upon domestic energy generation, manufacturing, water regulations and the Executive Branch provisions of the Inflation Reduction Act (IRA). This administration’s actions so far have been in line with our expectations, as discussed in our recent Public Policy Updates. Among the President’s stated goals are to “get America back on track” by implementing pro-growth economic policies, reducing bureaucracy/unnecessary regulation, allowing Americans to keep more of their hard-earned money, revitalizing manufacturing, reshuffling American foreign policy and renegotiating trade arrangements through the threat of tariffs and hard-nosed negotiating tactics.

Q1 brought tremendous change in terms of people, policy and priorities. Among those changes was the withdrawal from the Paris Climate Accord and redirecting the Energy department to focus on an “all of the above” energy strategy that would provide ample power to fuel America’s growth (and at lower cost). Other statements and policy initiatives focused on wind power, including pausing all offshore and federal land leasing, as concerns mount about bird strikes and whale deaths. EV purchase subsidies are at risk of being eliminated or significantly curtailed too. On the growth side, new policies are being put in place to benefit (a) farmers; (b) domestic manufacturing of solar panels, automobiles, semiconductors, steel, aluminum, pharmaceuticals and other products; (c) mining of critical minerals; (d) timber production; (e) domestic energy production (including liquified natural gas ports to benefit our allies in Europe and Asia); (f) shipbuilding; (g) cryptocurrency markets and (h) artificial intelligence advancements. And of course, there was DOGE. That is a lot of change in 70 days!

Stock market investors don’t like uncertainty about things like earnings growth, trade policy, tax rates and interest rates, so of course volatility spiked during Q1. That uncertainty also may have paused some of the M&A and IPO exit activity expected in 2025. However, with the recent IPOs of Kestra (cardiac medtech) and CoreWeave (AI cloud services) and Google announcing its $32 billion acquisition of Wiz (cybersecurity), there is evidence we are trending toward the healthier exit activity that many of us were predicting late last year.

Despite all the noise and uncertainty caused by the new administration, the outlook is strong for existing investments and the pipeline of new investment opportunities for both our strategies. The buyer’s market for impact secondaries continues for our newer funds and liquidity is on the horizon for our more mature funds. With respect to our infrastructure funds, the existing portfolio of renewable natural gas, hydro, energy storage and specialty solar projects are performing well and don’t appear weakened by new policy initiatives of the White House. The first investments in SIF IV are performing well and the pipeline of new opportunities is terrific. Importantly, we have no wind projects in our existing portfolio or in our pipeline, due to our long-standing caution regarding public policy and challenging risk-return dynamics in that sector. In sum, beneath the froth on the surface, there is calm and optimism in the investment sectors we address.

Announcements

25th Anniversary. In March, we marked the 25th anniversary of the formation of North Sky Capital. Press release here. During this time, North Sky launched the first impact fund of funds in North America (2005), the first sustainable infrastructure fund focused on the triple bottom line of attractive returns, renewable energy and jobs creation in the US (2010) and the world’s first impact secondaries fund (2013). To date, we have invested $1.5 billion across 200 impact investments. Thank you to everyone who has invested with us over the years and to our current and former employees, advisors, investment committee members and others who have played important assisting roles along the way. We could not have done all this without you!

New Mail System. We switched to a more robust email distribution platform for our quarterly market commentary and hope you like it. Please add the email newsletters@northskycapital.com to your “safe senders” list. Improved features include:

- click-thru navigation enabling you to jump from the table of contents directly to that section in the commentary and

- links to additional information on our website such as private pages containing data only for our readers.

SIF IV Update. Sustainable Infrastructure Fund IV has made two investments and a third is pending (spanning energy storage, community solar and EV charging). Its first investment was valued at 1.41x net MOIC (energy storage projects) as of yearend. We currently have co-investment opportunities for the 1st and 3rd investments – please contact Adam Bernstein if you are interested in participating.

CG VI Update. Clean Growth VI closed three new investments in Q1 and approved three more that are expected to close in Q2. We have committed about 75% of the fund’s capital to date.

Market Update

Yearend Insights. As secondary volume has increased over the last decade, so too has the number of investment banks and brokers that focus on secondaries transactions. Many of them conduct yearend surveys or publish annual reports. Below is our distillation of the various reports and datapoints for the 2024 calendar year:

1. Volume. Global secondaries volume for 2024 was $160 billion, up from $110 billion in 2023 and $115 billion in 2022.

• LP-led deals made up 55% of volume, with GP-led deals accounting for 45%.

• Dry powder is still less than two years’ worth of transaction volume.

2. Discounts. LP-led discounts decreased in 2024 (i.e., prices moved closer to NAV).

• Pricing for venture funds averaged 75% of NAV per Jefferies, although PJT data shows venture secondary pricing was in the range of 64-69%.

• Pricing for buyout funds was 94% per Jefferies.

3. Competition in Buyout Fund LP-led Deals. Several large ’40 Act secondary funds were raised in 2023 and 2024 and were rapidly deploying capital, mostly in buyouts. The consensus view is these new ’40 Act funds drove up pricing in buyout transactions by approximately 400bps. A skeptical view of these ’40 Act funds is the managers of them are more concerned about the consistent management fees they can generate by raising big funds than they are with making smart investments that perform over the long-term. Interests of ’40 Act fund managers are not as tightly aligned with LPs as other secondary managers, where carried interest (success fee to the manager) plays a substantial role in investment selection

4. CVs are Here to Stay. Recently, new fund formation in secondaries has been concentrated in single asset continuation vehicle (“SACV”) strategies. Several well-established control-oriented private equity firms have bolted on new SACV strategies, including Leonard Green, Accel-KKR, Audax, New Mountain and Warburg Pincus. They are essentially treating the growing market for SACVs as a new branch of the private equity tree—we agree. To be clear, these vehicles are being formed to invest in continuation vehicles sponsored by other firms (e.g., Leonard Green is not lifting companies out of its own portfolios). We believe there is plenty of room for these new entrants, and it validates that continuation vehicles are not merely a short-term fix to the drought in exits for private equity investors.

5. Beneath the Surface. While the above data points for the broader secondary market are helpful, there is more than meets the eye—particularly for specialist secondary managers like North Sky. For instance, most of our LP-led opportunities are in venture and growth equity funds. The LP interests we acquired in Q1 were purchased for 58% of NAV, which is more attractively priced than the Jefferies and PJT data shown above (75% and 64-69%, respectively). We believe this is due to very limited competition for impact deals and the reach of our proprietary deal flow networks. We also underscore that the focus of the new ’40 Act secondary funds is on acquiring LP interests in buyout funds. Therefore, the upward price movements they are causing don’t affect us.

Cautionary Tale on Pricing. Valuations for venture and growth equity companies (and others) has been shaky ever since the Fed intervened with 5.25% worth of fed funds rate increases starting in March 2022 and ending in July 2023. Valuations of such companies plunged as investors used higher discount rates to value their future cash flows. Many of those companies were not yet profitable, needed to raise additional capital to fund their growth and were facing the prospect of raising “down rounds,” where the valuation of the current round is priced lower than the previous round. Some of those down rounds were not priced low enough!

For example, a subsidiary of Munich Re recently announced it was acquiring venture-backed Next Insurance for $2.6 billion. Next had raised more than $1 billion since inception, with its most recent Series G financing completed in late 2023 at a $2.5 billion post-money valuation. The prior round (Series F), was completed in early 2021 at a $4.0 billion post-money valuation. Series G investors were likely expecting a 2-3x return on their investment but probably received something in the 1-2x range. For the record, we are not investors in Next. We are using it solely because the pricing data is publicly available.

Many private companies are still over-valued from the ZIRP-era. The key takeaway is buyer beware: there is no guarantee the valuation at exit will be sufficiently higher (or even higher at all) than the last round’s valuation such that a good return is achieved. The last round investors may not control the timing, valuation and ultimate decision about when the company is sold. You should not rely upon the last round investors having enough influence to assure an outcome above the last round’s valuation. We are very cognizant of this pricing situation at North Sky and can take proactive structuring steps to avoid a surprise outcome like this when necessary. We especially caution individual investors seeking to buy private company stocks on private market exchanges where full information disclosure and transparency may be extremely limited and the shares being purchased are behind a material preference stack, the terms of which may not be known to the buyer. Without full disclosures and a proper due diligence analysis, purchasing these shares seems inherently risky and/or speculative.

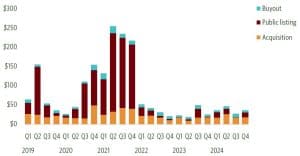

Exits. There has been a well-known dearth of M&A exits and IPOs for private equity investors in recent years, and we have discussed it in previous market commentaries. Let’s focus briefly again on IPOs.

Lack of IPOs Keeps Exit Value Low

Quarterly VC exit value ($B) by type

Source: Pitchbook-NVCA Venture Monitor as of December 31, 2024

We have not seen a large volume of IPOs since 2021, but it feels like that is about to change. As stated in the intro, Kestra, CoreWeave and other recent IPOs may be helping to re-open the IPO window. Further, companies like Klarna (consumer lender for “buy now, pay later” situations) and StubHub (online ticketing for entertainment events) are waiting in the wings for their IPOs. CoreWeave, with its AI cloud services focus, may lay the groundwork for an eventual IPO of Crusoe Energy, a portfolio company of North Sky. Crusoe’s AI-optimized data centers can use renewable power (wind, solar and geothermal) or waste natural gas that would otherwise be flared from oil fields. Notably, Crusoe is building the first data center as part of the $500 billion Stargate Project between Open AI, SoftBank and Oracle.

Sector Selection is Key. North Sky’s direct infrastructure investments experienced one of our stronger recent quarters in Q1 despite, and in part because of, the macroeconomic and policy changes described in the Introduction. President Trump’s Executive Orders pertaining directly to energy were all issued in his first wave of orders on January 20. Those orders were entirely consistent with our expectations, as discussed in our Policy Updates both before and after the election.

Exposure to the right sectors remains as important as ever. Upon passage of the IRA, North Sky, like many investors, spent considerable time canvassing the nascent clean hydrogen market for opportunities. However, over the past two years we remained cautious about deploying investor capital in this sector due to still-developing rules and regulations which we have shared in prior Policy Updates. On January 3, 2025, the Treasury Department announced final rules for Section 45V clean hydrogen tax credits, including stringent requirements for hydrogen-manufacturing technology whereby only specific types of renewable power may be used. While the final rules provide important guidance, we remain cautious about investing in the hydrogen sector today and see more attractive risk-return opportunities in storage, waste-to-value, grid optimization, community/specialty solar, EV charging and renewable fuels. It is also worth noting we have begun to see new opportunities to acquire renewable assets across all sectors and pricing has moved in our favor due to uncertainty surrounding the IRA, energy policy and tariffs on equipment like solar panels and batteries.

Energy Storage. North Sky allocated more capital to battery storage in Q1 than any other sector. Batteries are increasingly playing a major role in the US electricity grid, storing electrons generated from solar and wind power and then dispatching them as needed. Grid-tied batteries solve many problems for the regional transmission operators who are responsible for ensuring a consistent supply of power to users. Batteries can:

- provide stability to the grid (load balancing);

- meet peak demand and alleviate the need to build more gas peaker plants; and

- help power the large number of data centers that are being built to provide the computing power required by increasingly sophisticated artificial intelligence systems like ChatGPT, OpenAI, Claude and Grok3.

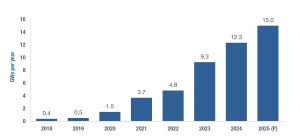

The US installed 12.3 GWs of new energy storage assets in 2024, according to Wood Mackenzie. As shown in the chart below, new energy storage installations have been increasing substantially each year since 2020, in part due to policy incentives and declining costs, which have reached a new low of about $115/kWh (Source: Bloomberg).

USA Energy Storage Deployments

Source: Wood Mackenzie

California has led the way thus far and now has about 15 GWs of installed battery capacity. California homeowners are also installing solar at a rapid clip. There were just 2 residential battery systems in California in 2010; today there are 193,000 systems (source: California Energy Commission). However, Texas overtook California in terms of new storage additions in 2024. Texas installed 6.4 GWs of batteries during the year, more than doubling its overall storage capacity. According to ERCOT, Texas may install more than 10 GWs of batteries in 2025, doubling installed capacity again! Other states have also begun installing grid-connected battery systems such as Florida, Idaho, Illinois, Maine, Massachusetts, New Jersey and New York—both red states and blue states. (Source: North Sky and US Energy Information Administration).

North Sky has played an active role in the evolution of batteries over the last 15 years, initially via our private equity/secondaries team funding technological advancement and commercialization; and more recently by our sustainable infrastructure team investing in battery projects in New York alongside our development partner Orenda Power. Most recently, the infrastructure team made an investment in the Texas marketplace alongside our development partner NewEdge Renewable Power. Texas offers a compelling investment opportunity today due to appropriate policy support, strong local demand, a booming economy, favorable business climate and quick grid interconnect times for new storage assets. For more information on our Orenda and NewEdge investments please see the Portfolio Updates below.

US Solar Milestone. In part driven by the domestic content incentives provided by the IRA signed into law by Joe Biden and in part due to the push by Donald Trump to onshore manufacturing of strategically important goods, more than half of American solar installations in Q1 are likely using panels manufactured within the US. The US has now surpassed 50 GW of domestic panel manufacturing capacity, over a 7x increase since 2020, and is now the world’s third-largest producer. Recent factory ribbon-cuttings in South Carolina and Georgia pushed domestic capacity over this threshold. Although China is still the world’s largest producer, in a short period of time the US will have transitioned from installing panels predominantly manufactured overseas to meaningful usage of domestically-sourced panels.

Domestic solar panel manufacturing holds significant political weight, as it not only generates jobs but also fuels demand for solar energy through sustained incentives for new development and construction. This surge in panel production aligns with robust domestic purchasing trends, evidenced by the installation of approximately 50 GWs of solar power capacity across the US in 2024. Historically, the US solar supply chain has relied heavily on foreign silicon ingots, wafers and cells, but this dependency is starting to shift. Efforts to localize production are gaining traction, highlighted by Mission Solar’s recent announcement to expand its San Antonio, Texas facility, enabling it to produce up to 2 GWs of polysilicon solar cells. We will keep tracking and reporting on these trends in future market commentaries.

Portfolio Updates. The first quarter of 2025 went well for our infrastructure portfolio. Building on the success of its first project sales on the last day of 2024, North Sky’s joint venture with Orenda Power saw continued momentum with the addition of four new development projects totaling up to 20 MWs into our portfolio in Q1, with another 65 MWs being evaluated for contribution in early Q2. This would bring the total portfolio close to 300 MWs of energy storage capacity. This portfolio continues to receive favorable results when bidding for offtake awards, indicating high demand in New York for battery storage.

North Sky’s renewable natural gas projects had strong first quarters of production. Our Victor Valley, California wastewater and organic food waste methane capture project setting a production record in March with over 20,000 mmbtu of RNG production. The favorable state-level California policies for RNG continued with the California Public Utilities Commission formally approving the first gas utility procurement required under the state’s Senate Bill 1440.

Additionally, our solar development affiliate, Paddle Energy, continues to advance its greenfield solar development efforts in Maine and Maryland. As of the end of Q1 2025, the portfolio totals approximately 50 MW of community solar projects in active development. During the quarter, Paddle also executed a letter of intent with a potential buyer for nine advanced stage development projects under favorable pricing. We expect the purchase and sale documentation to be finalized in Q2, with the projects being sold as each project reaches the Notice to Proceed milestone, scheduled to be between Q2 2025 and Q2 2026.

Sustainable Infrastructure Fund IV. SIF IV is off to a great start. Its first investment, an upsize of North Sky’s existing commitment to our partnership with Orenda Power in Q3 2024, has already appreciated significantly due to the growth and progress described above. Orenda will help New York meet its goal of zero-emissions by 2040. We are pleased to announce that SIF IV also completed its second investment, a newly-formed joint venture with NewEdge Renewable Power that will develop two portfolios: approximately 100 MWs of community solar projects in multiple states, and a 1 GW portfolio of energy storage projects in Texas. Both sets of projects are in the favorable energy infrastructure sectors we have identified, and the solar projects are already under contract to be sold to a long-term owner upon completion of their development. Like other North Sky developer relationships, the NewEdge team is experienced, focused on specific regional markets and was originated through our proprietary network.

SIF IV also signed a term sheet for its third investment, a portfolio of EV charging projects in a region that is not dependent on ongoing federal incentives. Importantly, these direct-current fast charging projects will immediately recoup up to 90% of installation costs via local programs. We also will have the opportunity to deploy complementary battery storage systems at each charging site. Note, SIF IV has immediate co-investment opportunities for the first and third investments, and we have a strong additional forward pipeline of deals in our preferred sectors. Please contact Adam Bernstein if you are interested in discussing these co-investments.

Industry Events. Our team participated in several conferences during Q1 as speakers and attendees, including the widely-attended Infocast Solar and Wind Summit, two regional conferences focused on power in the Mountain West and Texas, the US DOE Energy Storage Financing Summit and the Kayo Women’s Energy and Infrastructure Conference. Based on our conversations with a wide variety of industry participants ranging from developers and asset owners to grid operators and regulators, our main conclusion was that earlier-stage solar and storage assets are presently discounted due to trade-barrier driven variances on expected future construction costs. This causes the project fail rate on earlier stage development assets to increase, lowering bids for those portfolios. Contrast that with late-stage assets, which are being offered at premium pricing because the equipment has been secured already (no tariff concerns), construction has begun and qualification for the various local, state and federal incentives have been confirmed. We will be opportunistic buyers if we see an appropriate situation. Other market sentiments included the resiliency of the renewable energy tax-equity market, which surpassed $50 billion of deal activity in 2024, and the expansion into solar development of many of the industry’s most experienced wind developers.

The Long View. The energy transition is a global, secular trend and underpins our SIF IV strategy. Global demand for energy is rising due to population growth, economic growth, urbanization, rising consumption in emerging markets, the steady adoption of EVs and the rapid growth of artificial intelligence and the associated power consumption of data centers. In 2024, there was over $2 trillion invested globally in the energy transition, and as shown in the chart below, there has been rapid growth in such investments over the last five years.

The First Two Trillion is the Hardest

Annual energy transition investment passed $2 trillion in 2024

![]()

The above chart was excerpted from the latest annual slideshow authored by Nat Bullard of Bloomberg New Energy Finance. Mr. Bullard’s latest work spans 200 slides. In addition, to the chart above, other slides that caught our attention were 77 (EU now gets more power from renewables than fossil fuel), 78 (stellar year for solar), 85 (Texas: wind, solar, batteries), 91 (global battery installations), 92 (California cumulative battery installations), 116 (EV sales), 119 (China EV sales overtaking ICE vehicle sales), 138 (1TW of li-ion batteries sold in 2024),141 (battery price declines since 2010) and 163-185 (artificial intelligence and data center charts that are very good).

Conclusion

Reflecting on 25 years of investing, through every possible combination of economic, market and policy environments, we are as excited as ever about what the future holds.