Introduction

We pressed hard through the summer and passed several new milestones.

Sustainable Infrastructure Fund IV. We initiated SIF IV and made the first investment— a series of energy storage projects that provide peak load shaving and power on demand in the NYC area. SIF IV continues our long-standing strategy of constructing energy transition assets in North America. Currently, the infrastructure team is focusing primarily on renewable natural gas, energy storage and community solar projects in the USA, given the attractiveness of those sectors and the incentives and public policy support provided by the Inflation Reduction Act. Other actionable opportunities in our SIF IV pipeline include: small wind (< 20MW), fuel cells, EV charging, microgrids, hydrogen fuel stations, hydrogen storage, geothermal, waste-to-renewable fuels, biomass, solar on landfills, solar power for data centers and converting CO2 from heavy industry into commodities like baking soda and calcium carbonate. SIF IV represents our 10th impact fund.

Policy Update. The infrastructure team issued another public policy update, including commentary on the upcoming Presidential election.

Clean Growth VI. The initial investments are off to a strong start, generating a 2.0x net MOIC and 83% net IRR as of 6/30/24. The investment committee approved additional investments in Q3 and if all close as expected, the fund would be roughly 65% invested/committed. The portfolio is well diversified across smart grid, water, energy transition, circular economy, industrial efficiency, mobility, healthy living, food, education and other sectors.

New LPs. We welcomed new investors from Brazil, Singapore, UK, Germany, the Netherlands and the Caribbean. We also forged new relationships with family offices, pension plans, insurance companies, foundations and wealth management platforms.

Promotion. We have promoted Danny Zouber to Co-CEO! Scott and Danny, in essence, have been sharing leadership duties for the last few years as our firm grew and as Danny shouldered more responsibility along with it. Danny joined the firm in 2006 but has been intertwined with our team since 2001 when we shared office space with him and the rest of the Piper Jaffray Ventures team at 800 Nicollet Mall in Minneapolis. Over the last 18+ years, his responsibilities at the firm have steadily increased, and he has played a pivotal role in fostering our culture of innovation, client service and teamwork. Along the way, he helped launch the first cleantech fund of funds in North America (2006), our sustainable infrastructure strategy (2010) and the world’s first impact secondaries strategy (2013) where he was the driving force behind its formation. He has been co-head of the secondaries team since inception and has served on the investment committees for every fund in that strategy, as well as in our infrastructure strategy. He also led the start of our Low Income Communities initiative in 2020, which allocates new market tax credits to underserved, mostly rural, communities through our National Impact Fund subsidiary. Please join me in congratulating Danny on being named Co-CEO! —SB

Hurricane Helene

We are saddened by the loss of life and terrible damage caused by the hurricane from the Gulf Coast through the Carolinas. We have several team members based in Asheville, NC and that area has been absolutely devastated. All team members are safe.

Market Update

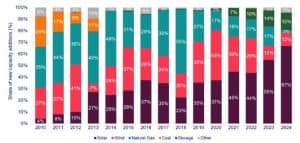

Market Update. During Q3, several members of our team attended RE+, the leading clean energy industry event. Over 40,000 industry professionals descended upon Anaheim for the 20th anniversary of this event. Attendance has doubled in four years, showing the remarkable growth and expanded interest in various solar power and adjacent sectors such as energy storage, hydrogen, wind, microgrids and EV charging. Last quarter, we highlighted key developments in the energy storage sector. This quarter we will focus on the solar sector due to its continued dominance in the energy transition landscape. During the first half of 2024, solar accounted for 67% of all new electricity generation capacity. Further, according to the Solar Energy Industries Association, the US solar market installed 9.4 GW of capacity in Q2 2024, a record second quarter for the sector. As another biproduct of the Inflation Reduction Act, US solar module manufacturing capacity expanded by over 10 GW to 31.3 GW in Q2 2024 as the industry pursues domestic content incentives and seeks to avoid exposure to an uncertain import tariff landscape.

New US Electricity-Generating Capacity Additions, 2010 – H1 2024

Source: Wood Mackenzie

The solar sector has also benefitted from a reduction in total system costs in what has otherwise been an inflationary environment over the last several years. Wood Mackenzie estimates that utility scale system pricing has dropped 2% year-over-year from 2010 through Q2 2024, driven by a steady decline in module pricing that has more than offset increases in balance of system (e.g., racking and tracking) and labor costs. Commercial and residential system pricing is down 12% and 6%, respectively, over that same period.

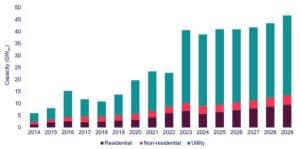

Looking forward, the US solar industry is on track to install over 250 GW in the next 5 years (2025-2029), growing total installed capacity to over 440 GW, demonstrating the role solar power is expected to have in the ongoing energy transition.

US Solar PV Installations and Forecasts by Segment, 2014-2029

Source: Wood Mackenzie

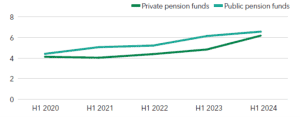

Playing Offense with Infrastructure. Infrastructure investing has historically played a bit of a defensive role in institutional investment portfolios, delivering steady returns in good times and bad. However, investors’ perceptions and expectations for infrastructure are changing. In part due to the massive global push for energy transition and decarbonization, and the public policy support thereof, infrastructure has outperformed private credit, private equity and real estate over the last three years. As a result, institutional investors have been increasing their allocations to infrastructure, as shown in the chart below.

Average Infrastructure Allocations Continue to Increase (%)

Source: Infrastructure Investor’s Investor Report H1 2024

Within private infrastructure, the middle market segment is attracting particular attention from investors. According to Goldman Sachs Alternatives, while approximately three-quarters of infrastructure transactions occur in the middle market segment, over 50% of the capital raised in 2023 was committed to large cap funds over $9 billion. Since the total mid-market infrastructure universe is valued at roughly $1 trillion, the relative underallocation of capital to these transactions represents a considerable opportunity.

The middle market also offers (i) the opportunity to invest in a highly targeted fashion (such as sector-specific GPs) and often to obtain co-invest rights and (ii) more exit pathways compared to large infrastructure investments due to a bigger potential buyer universe (i.e., more groups can handle the smaller ticket sizes of the middle market and exits can range from debt recaps/refinancings to sales to other infrastructure funds, municipalities, public funds, pension plans and insurance companies).

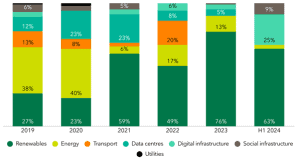

For sector-specific infrastructure funds, renewable energy has been the dominant global sector the last four years, dwarfing other sectors like transport and traditional energy.

Proportion of Sector-Specific Funds (%)

Source: Infrastructure Investor’s Investor Report H1 2024

We believe North Sky’s middle market, sustainable infrastructure strategy is poised to benefit from these factors.

Portfolio Updates. Q3 saw continued growth in North Sky’s joint venture with New York state battery storage developer Orenda Power, culminating in an expansion of our investment in the form of an upsized $10 million commitment from our latest infrastructure fund, Sustainable Infrastructure Fund IV (SIF IV). Alongside the new commitment, Orenda contributed an additional 10 projects, totaling 50 MW/ 200 MWh to the joint venture. Our third infrastructure fund (SIF III) saw continued progress at its renewable natural gas facilities, including the signing of a term sheet to provide significant RNG volumes to a large gas utility.

Buyside Observations

- It is a good time to be a secondary buyer.

-

-

- IPO and M&A exits remain muted, spurring investors to tap into the secondary market to generate liquidity. Pitchbook recently reported that the ratio of private equity exits to new private equity investments (i.e., money returned to LPs vs new money in) was 0.36x for the first half of 2024.

- While there has been growth in the number of buyers and their available dry powder (e.g., a handful of new ‘40 ACT funds), that growth seemingly still lags the potential supply from sellers.

-

- Global secondary sales volume is up 58% in 1H24 compared to the prior year (Source: Jefferies).

- While we have not materially adjusted our exit timing or valuation expectations for investments under consideration, the Federal Reserve’s 50 basis point cut to the fed funds rate in September is a positive development for both venture companies (supports higher valuations for high growth companies) and cash flow positive companies (lower interest expense on floating rate debt).

- We anticipate there will be an attractive and balanced mix of LP- and GP-led opportunities in the quarters ahead.

-

-

- LP-led opportunities will be driven by institutional investors that are seeking to monetize older positions to fund new investments and maintain vintage year diversification. We expect an increase in deal flow for 2017-2020 vintage years funds given their lack of distributions to date and sideways progress. Per Carta, approximately 33% and 43% of 2017 and 2018 vintage funds, respectively, have yet to make a single distribution to LPs.

- We expect GP-led opportunities will be a mix of multi-asset tail-end solutions for old funds and single-asset opportunities for trophy assets offered by experienced GPs.

-

Exit Environment

- We are seeing more fund managers explore exit opportunities for their portfolio companies, including strategic sales, sponsor-to-sponsor sales, IPOs and continuation vehicles. The key word is “explore.” Most managers we speak to are actively engaged in exit readiness programs for their aging investments but are still waiting for either 1) more clarity in the regulatory or political landscape in Q4 or 2) more favorable asset pricing that comes with lower interest rates and a risk-on investor mentality. Manager consensus is we are heading for a more favorable exit environment in 2025.

- US private equity exits during 2023 reached a record high median holding period of 7 years (Pitchbook).

- A few takeaways from recent conversations with investors, allocators and industry advisors:

-

-

- Managers continue to selectively seek exits for their largest and presumably best performing assets, while strategic acquirers continue to be the buyer of choice despite the regulatory headwinds that exist for some of the largest corporations;

- In our estimation, a decline in sponsor-to-sponsor exits is partially attributable to the rise in continuation vehicles that allow a sponsor to retain an asset rather than sell it to a competitor; and

- The stock market has performed well year-to-date and select companies are going public, yet most have shelved their IPO aspirations until 2025 when the US elections will have passed and the Fed may have made more than one rate cut.

-

Continuation Vehicles. With each passing quarter, North Sky is seeing more attractive continuation vehicle opportunities. Pre-Covid, GP-led deals were roughly 33% of the secondaries market. As Covid set in, price uncertainty drove bid-ask spreads to extremely wide levels for traditional LP secondaries. The market responded by shifting to GP-led deals. Per PJT, GP-led deals rose to 55% of all secondary transaction volume in 2020 and stayed elevated until last year when they fell back to 42%. Given the attractiveness of continuation vehicles and the market’s acceptance of them, PJT believes the trend line will again reverse. We agree. See the two following charts.

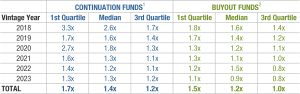

Continuation Funds Have Demonstrated Strong Absolute and Relative Performance

Net MOIC by vintage year

Source: Morgan Stanley and Preqin as of December 2023 and publicly available information. Past performance is not indicative of future performance.

1 Dataset represents 71 continuation funds with vintages between 2018 and 2023

2 First quartile boundary, median and third quartile boundary return benchmarks are calculated using performance data from Preqin’s database comprising of 696 buyout funds with vintages between 2018 and 2023.

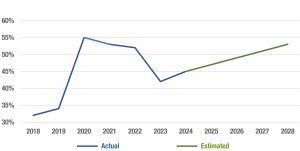

GP-Led Deals as a Percentage of Total Secondary Market Transaction Value

Source: PJT

Conclusion

It was another busy quarter and the next signpost ahead is the US Presidential election. Stay tuned.