INTRODUCTION

There is a lot going on in the world—lots of news and noise—but let’s stay focused on the tasks and opportunities at hand. We are in the first inning or two of the age of AI and already seeing its benefits in areas of physics, chemistry, biology, medicine, robotics, manufacturing, energy generation, mobility, communications, education, food and housing. Every sector we are investing in will be affected by AI, accelerating growth, extending the envelope of what is possible and enhancing efficiency and efficacy. CG V and VI had a terrific second quarter (valuation gains). Our secondaries team and our infrastructure team put new capital to work in very attractive deals. Our deal flow has stepped up recently, especially for our secondaries team as some of the chaos/noise begets opportunity (more on this below). We see new challenges emerging too, such as how will we sustainably power the massive data centers needed for AI and how will we keep the robots and other technological wonders from killing or enslaving us as portrayed in books and movies like 1984, the Terminator, War Games and Minority Report, to name a few. It seems some politicians need to be reminded that Orwell’s most famous work was a warning, not a “how to” guide. But I digress.

There has been so much positive news and technological progress in our sector coverage areas during the quarter, it would be impossible to list them all here, but below is an illustrative sample:

Solar. We are moving into a world of do-it-yourself solar power where anyone can plug solar panels into an electrical outlet to help power their home or apartment—no electrician required. This summer, IKEA began selling balcony solar kits in Germany that offset grid-provided electricity usage with electricity produced by the panels. Basic packages include two 520W panels, an inverter, mounting brackets and power cords for about $530. A larger version, priced at $2,300, has four solar panels and a battery to help time-shift energy production to match energy consumption. By some estimates, two 520W panels might cover 35% of the electricity needs of a typical European apartment, so the impact could be significant if widely adopted.

Mobility/Cars. We continue to move toward full self-driving cars. Waymo offers driverless taxis within geofenced areas in Atlanta, Austin, Los Angeles, Phoenix and San Francisco and is currently making about 360,000 weekly trips (a 7x increase from May 2024). Tesla now offers robotaxi services (still supervised by a human) in parts of Austin and San Francisco to San Jose. Zoox (backed by Amazon) does the same in Las Vegas and San Francisco, and Pony.ai is piloting similar projects in China, Dubai, Singapore, South Korea and Luxembourg. Regardless of the recent expiration of the $7,500 tax credit, EVs are generally becoming the low-cost choice for many buyers, compared to gas-powered vehicles. Not only are prices of new EVs getting more affordable (e.g., the sub-$30k Nissan Leaf and lower priced models being announced by Ford, GM, Rivian, Slate, Tesla and Toyota), but car buyers have been flocking to used EVs thanks to attractive pricing and fuel and maintenance costs that are roughly half of gas-powered vehicles. Anecdotally, the first legitimate electric RV just debuted in Elkhart, IN. The Coachmen RVEX is 24’ long, AWD, has a range of 270 miles, 1,000 W of rooftop solar and price of $150,000. It is built on Chevrolet’s Bright Drop EV chassis.

Batteries. LG Energy Solution made a huge breakthrough in lithium metal battery technology by creating a new electrolyte that inhibits the formation of dendrites during fast charging. Lithium metal batteries have greater energy density (more power, less weight) and longer lifespans than today’s lithium-ion batteries, but lithium metal batteries must be charged much more slowly. This discovery overcomes that hurdle, enabling a much lighter battery capable of powering a car for many years (nearly 200,000 miles) with a 500-mile range per charge and a recharge time of just 12 minutes. Earlier this year, BYD announced its megawatt flash charging technology, which supposedly can charge an EV in half the time of the latest Tesla superchargers. BYD can give you 250 miles of range in five minutes but requires very expensive 1,000-volt chargers. On a separate note, Tesla announced its Megapack3, an upgraded energy storage system capable of 5 MWh of power vs. the 3.9 MWh from the previous model. It uses the latest cell technology supplied from the US, SE Asia and China and has a significantly simplified, more reliable design with improved fire protection. Our infrastructure team uses Megapack systems in its Orenda projects in New York.

Market Update

Intentionality / Additionality. North Sky’s investment strategy is highly intentional and creates new (additional) impact benefits. We are not simply buying LP interests in existing impact funds at steep discounts but rather providing new growth capital through (a) structured investments, (b) single- and multi-asset continuation vehicles, (c) primary commitments and (d) other ways discussed below. This allows us to deliver the impact results institutional investors are seeking today.

Intentionality: Every investment we make is meant to be impactful. CG VI is our 10th impact fund and we have become pretty good at this over the last 20 years. We make investments that align with, and positively contribute to, the United Nations Sustainable Development Goals (“SDGs”). All our portfolios are mapped to the SDGs (and the underlying Target Indicators). Impact info is reported quarterly to our LPs. We also publish an annual impact report (and have been publicly doing so since 2012). Further, we monitor impact by tracking the key performance indicators of portfolio companies and how their intended outcomes support the goals. Portfolio diversification typically spans climate, energy, mobility, water, waste, food, healthcare, education and the other areas.

Additionality: There are three important levers. First, we perform an ESG check and risk scan prior to investing, which creates an opportunity to “nudge” the investment target regarding ESG factors and our desire to promote the adoption of ESG-focused actions and recommendations. For investments that already have an impact mindset, our nudge may result in renewed efforts by company leadership to deliver impactful results, enhanced data collection/reporting or a broader scope for tracking key performance indicators. For investments that were not originally made as overt impact investments, our nudge typically bears even more fruit, as we shift the mindset of company leadership to be intentional about the impact they can achieve and to measure that impact using key performance indicators. Second, our capital supports the growth of impact companies. It is most pronounced when we are participating in continuation vehicles and structured transactions (e.g., preferred equity structures) but also happens via traditional secondaries (through additional capital calls on unfunded commitments), seasoned primaries and secondary directs, where we often end up in direct dialogue with the company’s executives which may lead to new growth capital opportunities for the fund or our LPs as co-investors. Third, our impact secondaries funds provide the global impact ecosystem with an exit option that did not exist prior to our first impact secondaries fund in 2013. An active impact secondary market (a) expands and strengthens the impact ecosystem by assuring new entrants there will always be an exit path and (b) enables existing impact investors to rebalance and channel impact capital into new areas as their priorities evolve. And—as discussed at the end of our Q2 market commentary—there is a lot of opportunity for us to expand this important clearinghouse function!

Liquidity, positive economic data and other tales from the sell side. Over the past few years, PE investors have been told “investment banks are being hired, companies are prepping for IPOs/M&A exits and next year will be a big year for liquidity.” Yet the timeline for exits seems to keep slipping, which means liquidity remains constrained, exits are especially tough for lower- and mid-tier companies and partial liquidity events are increasingly common. The chart below shows US IPO volume is trending upward but still off from 2017-2021 years.

US IPO Market

IPOs ≥ $50mm Mkt Cap

Source: www.renaissancecapital.com as of 9/30/2025

Global M&A volume also appears to be on the upswing, with early reports from Dealogic for Q3 showing a stunning $1.26 trillion in volume—up 40% year over year. Based on data available to us from Pitchbook and Dealogic 2025 may be on pace to exceed $4 trillion in volume, perhaps as much as $4.38 trillion. Over the last 10 years, only one other year exceeded $4 trillion—2021 tallied $4.75 trillion in global M&A volume per Pitchbook. That’s encouraging.

Beyond IPOs and M&A, we see other positive signals. Inflation has moderated, the S&P 500 is up 14% YTD, debt markets are active and interest rates have stabilized and are benefiting from the recent Fed Funds rate cut. Recent liquidity examples within our funds include Eli Lily’s purchase of Scorpion Therapeutics (CG IV), DENSO’s purchase of Axia Seeds (CG V), Mitsubishi Electric’s purchase of Nozomi Networks (CG V & VI) and dividend recaps at Energy Solutions (CG V) and Bristol Hospice (CG V). We are aware of several other significant liquidity events on the horizon for our Clean Growth funds.

We anticipate liquidity over the next year will be concentrated in high-quality companies that are sold at reasonable multiples (i.e., lower than the 2021-2022 peak valuations) and low-quality companies where managers dramatically lower reserve prices to close the book on an underperforming investment. The prime exit window for medium-quality companies will follow in 2027-2028.

Buyside considerations (new investments). After a brief pause when US tariffs were announced this spring, secondary activity roared back to life. First half secondary volume according to Evercore, PJT and Jefferies was in the $100-105B range. As second half volume is typically larger than first half, we believe secondary volume will surpass $200B this year for the first time. Transaction volume is relatively balanced between LP-led and GP-led secondaries. The former being a transaction where one investor steps into the shoes of another without affecting the underlying investment structure of the asset being acquired. The latter being a transaction in which investment objectives and economics are re-set with the general partner in a manner that provides the original investors an option to cash out or roll their investment forward. Yale, Harvard and other college endowments were notable sellers of large private equity portfolios in recent months, although our interaction with corporates, pensions and family offices suggests all investor types are actively seeking secondary solutions today. Our friends in the brokerage community tell us a growing share of secondary sellers are first timers. To us, these are good indications of a healthy, maturing market where secondaries are no longer a one-off transaction but rather becoming an important portfolio management tool investors use to maintain a balanced portfolio and generate liquidity when needed.

Our impact secondaries strategy focuses on companies that are not dependent on policy support to grow or achieve profitability, so our secondaries investments have been little affected by the One Big Beautiful Bill Act (“OB3”). We also prioritize diversification across a multitude of environmental and social impact themes, so any negative change within one subsector will not have an outsized effect on the overall portfolio. Looking forward, we see a broad universe of investment opportunities spanning smart grids, circular economy, industrial innovation, climate adaptation & mitigation, smart cities & transportation, food systems, renewable energy, healthy living & aging, financial inclusion and education. We continue to have almost no direct competition in the impact secondary marketplace and believe this sector has tremendous growth potential. We are on pace to put $100M to work in impact secondaries in 2025, but this market could easily support more than 10-20x that amount right now and perhaps as much as 100x that in a few more years.

Sustainability meets AI. The initial release of ChatGPT in November 2022 catalyzed a wave of investment in AI related technology companies. For those focused on impact investing, many have chosen to participate in this hot market by supplying the power needed for data centers to run these energy intensive technologies. The dirty secret is these data centers require a lot of backup power, which is commonly provided via diesel generators. Deloitte is forecasting that by 2035, AI data centers will increase their power usage by 30x from their 2024 levels. The fastest way to meet these power demands is by using renewable energy (e.g., wind, solar and battery storage), where construction timelines are often less than 2 years vs. about 5 years for a new natural gas plant and even longer for nuclear. Recently, CG VI portfolio company Crusoe Energy teamed up with battery recycler Redwood Materials to quickly and economically deploy about 800 repurposed EV batteries at a large data center managed by Crusoe. The battery array serves as backup power and can also be used to time-shift electrons coming from renewable energy systems. Batteries can be swapped out as performance degrades without shutting down the whole system. This approach can be deployed up to two times faster and at roughly half the cost.

Power demand. We have written extensively about the generational increase in US demand for electricity since 2023, and that trend continues as a key macro investment factor. The federal Energy Information Administration recently forecast US power consumption will hit new highs of over 4.1 million megawatt-hours in 2025 (2.3% annual increase) and 4.3 million megawatt-hours in 2026 (3.0% annual increase). Note this compares to less than 1% average annual growth from 2005-2022. Each additional percentage point of annual demand growth represents billions of dollars of incremental power infrastructure requirements.

These increases were driven by data center expansion, continued conversion of household energy from fossil fuels to electricity and cryptocurrency mining. Renewable electricity is expected to provide the largest portion of the new power generation that will be installed to meet this demand. Further, renewable energy now provides roughly 25% of total US power generation. We have come a long way from the days of calling this sector “alternative energy.”

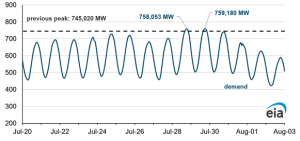

Supporting the EIA’s forecast, this summer saw new record high “coincident peaks,” which is the maximum demand for electricity during a given hour. These peaks are significant because they drive both commercial and regulatory planning for capacity additions and resiliency requirements.

2025 Hourly Electricity Demand for the Lower 48 States

thousand megawatts (MW)

Source: U.S. Energy Information Administration, Form EIA-930, Hourly and Daily Balancing Authority Operations Report

As one component of the larger demand story, and relevant to North Sky’s infrastructure projects in Maryland and Ohio, the PJM Interconnection—the electric grid spanning the mid-Atlantic and eastern Midwest—set a record high for its recent capacity auction. Capacity auctions are conducted by regional electric grid operators to secure future power supply to meet forecast power demand. PJM’s Base Residual Auction for delivery in Years 2026/2027 recently cleared at $329.17 per megawatt-day, a 22% increase over the prior year’s auction. Further, the forecasts which informed the clearing price INCLUDED the expectation that 1,100 megawatts of power capacity that had previously been slated for retirement would postpone decommissioning and remain active.

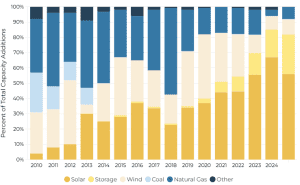

Solar and storage deployments continue to dominate. For 2025, the EIA forecasts solar electricity will again make up more than half of all new generating capacity added to the US grid. Other notable movements are energy storage counting as more than 20% of new additions and a resurgence in natural gas, which is likely in response to voracious power demand from data centers (expansion and new construction).

U.S. Annual Additions of New Electric Generating Capacity

Mackenzie Power & Renewables US Solar Market Insight Q3 2025; EIA

OB3 update. In Q3, the renewable energy sector experienced expected shifts in business plans and procurement strategies following the passage of OB3 on July 4. Our prior market commentary outlined the bill’s key provisions, noting that the changes were less disruptive than many media headlines implied.

RE+ conference. In September, our infrastructure team attended the RE+ conference, the largest annual gathering of renewable electricity companies in the US. There were 37,000 participants this year. We engaged with numerous developer and industry partners, and a key takeaway was the sustained enthusiasm from lenders and other capital providers for investing in renewable infrastructure, including projects within our funds. While some attribute this interest to impending ITC deadlines, our experience suggests that banks and capital providers, who dedicate significant time and diligence to underwriting long-term commitments, are not merely reacting to short-term incentives but anticipate continued market growth.

The enthusiasm was not universal within the infrastructure ranks. Several large well-known development companies experienced distress in Q3, with some going into bankruptcy. Some of them were dependent on a steady pace of new construction within a tight range of costs across a portfolio of large, levered projects in multiple regions. OB3 created tremendous cost pressure, and some developers could not withstand it. To wit, if a development company employs many construction workers, the expense of even a small delay can be disastrous. The workers need to be paid even if they are not building anything. Solar developers within house construction teams are reminded of this important lesson every few years. North Sky Infrastructure’s middle market strategy, investing in discrete markets with small and medium-sized developer-operator partners, has avoided any post-OB3 distress.

Portfolio updates. So much for a quiet summer! In response to the OB3’s incentives for “safe-harboring” power generation equipment, our solar and battery storage portfolio partners either executed, or will imminently execute, long-lead equipment orders. These purchase orders allow final completion for projects to occur after the new statutory deadlines in OB3, as well as allow equipment procurement to occur pursuant to the existing regime of Foreign Entity of Concern (“FEOC”) rules regarding overseas imports.

Paddle Energy sold one of its community solar projects in Maine on very attractive terms in Q3. Paddle performs solar development and related work for the benefit of our third fund, Infrastructure Investment Fund (“IIF”). NewEdge Power, a solar development partner for Sustainable Infrastructure Fund IV (“SIF IV”) made progress toward selling multiple projects as well. Our SoCal Biomethane renewable natural gas project in San Bernardino, CA advanced its regulatory approval process with the California Public Utilities Commission, moving closer to securing the second long-term RNG offtake agreement under California’s Senate Bill 1440.

During the quarter, we also negotiated term sheets with two more solar development teams, one for IIF and one for SIF IV. We believe both teams will take advantage of the opportunities created by the policy changes made by OB3 and the surge in power demand from AI/data centers, EVs, residential homeowners and businesses.

Opportunity Zone program extension. Our third infrastructure fund, IIF, develops sustainable infrastructure projects within Opportunity Zones, which were promulgated under the 2017 Tax Cuts and Jobs Act. That Act was intended to incentivize investment in lower-income areas. A lesser-known aspect of OB3 is the permanent extension of the Opportunity Zone program, previously set to expire in 2027 for new qualifying investments. OB3 also enhanced the incentives for investing in rural areas, now offering a 30% basis step-up to reduce capital gains taxes after a five-year holding period. While IIF is nearly fully committed, increased market interest in new OZ investments has improved long-term liquidity prospects for the IIF portfolio.

Conclusion

Q3 2025 showcased a dynamic landscape for impact secondaries and sustainable infrastructure, driven by robust deal flow, technological advancements and strategic adaptations to policy shifts like OB3. Our Clean Growth Funds V and VI delivered strong valuation gains, while new investments capitalized on emerging opportunities in water treatment, data center cooling, supply chain logistics, urban mobility, chronic care management and personalized learning. Our infra team continues to see terrific investment opportunities within community solar and energy storage. The RE+ conference underscored sustained investor enthusiasm, reinforcing the sector’s growth trajectory. As we navigate challenges like liquidity constraints and rising energy needs, North Sky remains committed to delivering attractive returns and impactful outcomes, aligning with our mission to foster a sustainable future while seizing the moment’s opportunities.