Introduction

Impact investors were jostled around in 2025 and some fared better than others. Midyear, our solar development team coined the phrase “Solar Coaster” to describe the ups and downs and twists and turns they were experiencing due to tariffs, geopolitics, executive orders, changes to the rules underlying the Inflation Reduction Act, the One Big Beautiful Bill, interest rates, the Fed, the rise of AI, state policy changes and wild price swings in solar panels, racking, inverters and batteries to name just a few. Some investors and developers did not survive the ride; while others thrived like we did.

During the year, North Sky focused on managing risk, staying on top of policy changes and positioning our funds for success, both in terms of achieving strong exits for our more mature holdings and finding attractive new investments. I have never been prouder of our team than I was this year. As we wrote about in our Q2 2025 Market Commentary, change begets opportunity. Both teams rolled with these changes and used the volatility to create investment opportunities for our funds, sometimes benefitting from the missteps or miscalculations of third parties. We rode through the challenges using creative problem solving, teamwork and our experience, relationships and market position. And there was never any doubt or complaining. We just said, “it is what it is,” and ground our way through it. In a sense, we made our own “luck” by taking action, appropriately managing risk and seizing opportunities when they arose.

North Sky had a great Q4 and a great year overall. We hit a big milestone:

- Exit Activity. The federal government was shut down for 43 days in early Q4, likely shaving a full percentage point from GDP and injecting new uncertainty into capital markets. This moved many hoped-for private equity exits sideways by yet another quarter. Despite this, we are happy to report that in 2025 we returned nearly one-quarter of all capital called from LPs over the last 12+ years in our Clean Growth program. Our sustainable infrastructure team also achieved multiple exits within our energy storage (Orenda) and community solar (Paddle) portfolios and this capital was recycled to fuel the growth of those joint development efforts.

Other noteworthy observations from Q4…

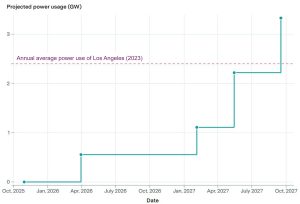

Energy Demand. We previously reported how global energy demand has ticked up recently, after moving sideways for much of the last decade. But with the shift to EVs and, more importantly, the parabolic increase in demand coming from datacenters due to AI, we are going to need more power. A LOT more. Case in point, Microsoft’s Fairwater datacenter in Mount Pleasant, WI, which will use hundreds of thousands of NVIDIA GPUs and span 315 acres. Construction will take place in four phases, with the first coming online in April 2026 and the final phase scheduled for September 2027. When fully operational, it is expected to consume 3.3 GWs of electricity—more than the city of L.A.!

Microsoft’s Fairwater Datacenter Will Use More Power Than Los Angeles

Source: EPOCH.AI and Alexa Capital’s Gerard Reid

Driving Record. In late 2025/early 2026, Tesla owner David Moss completed a significant milestone by driving from Los Angeles to Myrtle Beach, South Carolina, using Tesla’s Full Self-Driving (FSD) Supervised software (v14.2) with zero disengagements, including parking and charging, marking a major step for supervised autonomous driving. While previous efforts (like Delphi’s 2015 trip with a safety driver) existed, Moss’s drive showcased the growing real-world capability of FSD in handling varied conditions, prompting discussions on the future of autonomous tech and regulations.

Flying Cars. Now that someone has traversed the USA handsfree in an EV, when will someone do the same in an eVTOL? Anduril’s founder, Palmer Lucky, recently purchased and flew a Jetson One electric vertical takeoff and landing (eVTOL) aircraft. The tiny, drone-like craft is made of aluminum and carbon fiber and has eight battery-powered electric motors, an auto-landing system and ballistic parachute. Flight time is only about 20 minutes but that is expected to improve. Cost: $148,000. Further, the US government just released a federal strategy to bring Advanced Air Mobility to American skies and American eVTOL companies like Joby are working in close collaboration to craft the regulatory framework to do this safely and to manufacture eVTOL aircraft and build vertiports globally.

Chemist Cracks America’s Rare Earth Problem. Rice University chemist James Tour has developed a breakthrough flash Joule heating process to recover rare earth elements (REEs) from electronic waste and discarded magnets. This rapid technique heats materials to thousands of degrees in milliseconds, combined with chlorine gas, vaporizes non-REE metals, leaving high-purity REE residues in seconds—without acids, water, or toxic waste. It cuts energy use by up to 87% and enables efficient recycling within US e-waste stockpiles. China dominates over 90% of global REE processing and magnet production, creating supply vulnerabilities for tech, EVs, renewables and defense. Mr. Tour’s method, licensed to Flash Metals USA, offers a fast, low-cost path to domestic independence, with commercial production targeted for early 2026. The innovation also applies to other wastes, turning environmental liabilities into resources and potentially reducing geopolitical tensions over critical minerals.

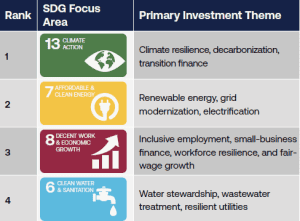

US SIF Report. US SIF released it latest report on December 9, 2025. Among its findings were that (1) US Sustainable assets under management rose slightly YoY from $6.5 trillion to $6.6 trillion and (2) investors are prioritizing the climate change, clean energy transition, economic growth and clean water & sanitation sectors.

Top SDGs for Impact Investors

Source: US SIF 2025 Survey

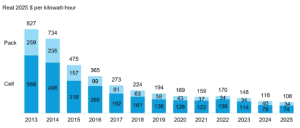

Battery Prices Fall Again. We closely follow trends within the battery sector as this is an important area of opportunity for both our impact secondaries and sustainable infrastructure strategies. Thanks to intense competition, economies of scale and an ongoing shift to lower cost battery chemistries like Lithium Iron Phosphate (LFP), battery prices continued to drop. Per BloombergNEF’s recently released 2025 lithium-ion battery price survey (and the excerpted chart below), battery cell prices are an average of $74 per kilowatt-hour. Battery packs, which include cells, housing, battery management system, wiring and a thermal management system, add $34 to the cost, bringing the total to $108 per kilowatt-hour. Pack prices have fallen from $827 per kilowatt-hour in 2013 to $108 today, which represents a 12.6% annual decline on average. Next-generation breakthroughs—such as silicon- and lithium-metal anodes, solid state electrolytes, advanced cathodes, and novel manufacturing processes—are expected to drive the next major wave of cost reductions.

Volume-Weighted Average Lithium-Ion Battery Pack and Cell Price Split 2013-2025

Source: BloombergNEF

Goldman Sachs Family Office Survey. A recent report from Goldman suggests family offices are increasing their investments in secondaries. 72% of respondents invest in secondaries in 2025 (up from 60% in 2023), valuing shorter duration and access to mature portfolios.

Market Update

Portfolio Updates. During the quarter, we made good progress toward to putting the remaining capital for CG VI to work. We expect to make the final investment for CG VI in Q1. Note, CG VI’s investments span multi-asset continuation vehicles (CVs), single-asset CVs, LP secondaries and preferred equity investments.

CG VI had significant recent portfolio realizations resulting in a November distribution of 12.5% of contributed capital. Since inception, the fund has distributed 23% of capital back to investors. A notable exit included in the November distribution was the sale of Adaxia I portfolio company Nualight to Fulham, which returned nearly 60% of CG VI’s cost basis and exceeded our base case expectations by 55%.

Elsewhere in our portfolio, several underlying portfolio companies returned capital to investors through excess cash flow or dividend recapitalizations that were made possible by material growth in revenue and/or profitability. These include CR Fitness, MMIST, Interface Biologics, Embriq, Project Sun, Bristol Hospice and EnergySolutions. We view these partial realization events as a precursor to a full exit event in the next 18-36 months. Several other companies, such as PPC and Aloha, are well positioned to be acquired in the near-term.

Exit Environment. In recent quarters the exit environment has steadily improved from the post-COVID M&A trough in Q3 2023. Despite the optimism and anecdotal comments from deal makers, investors have been underwhelmed with the depth and breadth of liquidity in their private market portfolio. Initial Q3 2023 M&A data from PitchBook suggests the long-promised exits may finally be materializing and represent the start of a more favorable exit environment. Measured by deal value, Q3 2025 global M&A increased 26% QoQ, 35% YoY and 78% from the post-COVID low in Q3 2023. Measured by deal count, Q3 2025 global M&A increased 4% QoQ, 19% YoY and 28% from the post-COVID low in Q3 2023.

While not widely reported, we have noticed an increase in M&A transactions that are subject to some form of regulatory approval. In certain cases, this has extended the timeline from deal announcement to close. Fortunately, we have not had an exit blocked due to regulatory approval.

Our list of potential 2026 liquidity events is expanding. Many of our funds’ top portfolio companies are hiring investment bankers and starting preliminary conversations with acquirors to flush out any potential preemptive acquisition offers. Most of these formal processes are scheduled for Q1 2026, which means our expectation of liquidity from them blooms in Q3. Recent conversations with underlying managers indicate they will use an improving exit environment to monetize investments that have underperformed the manager’s expectations. In many cases, these are situations in which a company either (1) has had declining or lower-than expected growth rates that makes its last round valuation ‘expensive’ in the current market or (2) needs additional capital or time that is not possible in the manager’s fund structure.

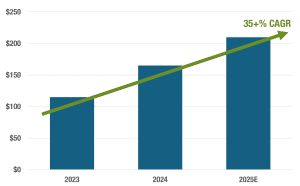

Buyside Considerations. The rebound in global M&A exits has not reduced secondary activity. PJT estimates that Q3 and Q1-3 secondary volume was $60B and $165B, respectively. At this rate, 2025 secondary volume is expected to be $210B.

Secondary Market Volume ($B)

Source: PJT Partners Q3 2025 Secondary Market Insight

Structure-wise, volume has been split 52% GP-led and 48% LP-led. On the GP-led side, we are seeing the build out of GP-led advisory teams at middle-market investment banks over the last two years is now leading to more single-asset continuation vehicles for lower- and middle-market sponsors who have not yet accessed the secondary market—which should lead to even more opportunities for our Clean Growth strategy. On the LP-led side, the number of programmatic sellers has continued to increase, as too has the number of first-time sellers. In our impact-niche, we would characterize sellers as those that have used secondaries in the “traditional” side of their portfolio and are now using it in the “impact” side of their portfolio. For GP-led transactions, we see many opportunities to partner with generalist managers on single asset continuation vehicles of inherently impactful companies. For multi-asset continuation vehicles, we are mostly seeing opportunities to partner with self-identified impact managers and corporate venture capital arms that have invested with an impact lens.

Looking ahead, we believe the dynamics are favorable for buyers of impact secondaries. Net cash flows for the venture industry continue to be negative, as they have been since 2021. The best performing private companies are not rushing for the exits. The PitchBook NVCA Q3 2025 Venture Monitor reports that more than 40% of unicorns raised their first venture round more than a decade ago and those unicorns that remain private have an aggregate valuation of more than $3.7 trillion based on their last round financings. Venture and impact fundraising continues to decline from the 2022 peak. As noted in PitchBook’s 2025 Sustainable Investment Survey, the current political environment in the US has resulted in 60% of organizations changing or evaluating their message on ESG. All these factors create uncertainty and anxiety for investors, which eventually leads to demand for secondary liquidity. As the first and most experienced impact secondary manager globally, we are in a great position to use these dynamics to create attractive risk-adjusted entry points for our investors.

Despite persistent negative headlines about renewable energy, we ended the year with stronger sector-wide momentum than last year.

Solar and Storage Dominates Renewable Generation. According to Wood Mackenzie, the US solar industry installed 11.7 GW of capacity in Q3 2025 (+20% YoY, +48% QoQ), and the third largest quarter for deployment in the industry’s history. Solar accounted for 58% of all new electricity-generating capacity added to the US grid through Q3, with more than 30 GW installed. Solar and storage, combined, accounted for 85% of new capacity. The “red-state thesis”—which posits that solar incentives have delivered significant benefits to Republican-led states, thereby fostering bipartisan support—has been proven once again. Of the ten states with the most newly installed solar capacity during the first three quarters of 2025, eight are (in descending order): Texas, Indiana, Florida, Arizona, Ohio, Utah, Kentucky and Arkansas. California and Illinois round out the list.

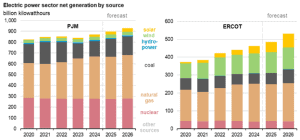

By now, our clients have read multiple North Sky reports on the rapidly growing demand for electricity, due to EVs and computing needs. This trend continued in Q4. Particularly relevant to our portfolio, the Energy Information Administration’s Energy Outlook for December cited the Mid-Atlantic/Ohio Valley region (known as “PJM” territory) and Texas (known in the power industry as “ERCOT”) as the fastest-growing areas for electricity use. As shown on the charts below, solar capacity within those regions is projected to expand 63% from 2024-2026 in PJM, and 92% during the same period in ERCOT. North Sky has investments in solar and energy storage projects in both regions.

Solar Generation Growth in Mid-Atlantic and Texas

Source: US Energy Information Administration

Electric Vehicles. As forecasted in North Sky’s policy research, EV tax incentives were curtailed by July’s One Big Beautiful Bill (OBBB). An expected surge in sales occurred in Q3 ahead of the September 30 deadline for buyers to secure a signed contract to qualify for incentives, followed by a sharp drop in Q4. However, the EV charging business has remained far more consistent. In Q4 the number of publicly available EV chargers deployed in the US exceed 230,000 for the first time, with increasing utilization and reliability. North Sky has been evaluating the EV charging infrastructure sector since 2021, and we have identified an attractive, risk-managed entry point with upside exposure to growth scenarios (see Portfolio Updates below).

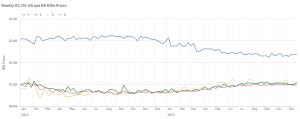

Renewable Fuels. Our previous market commentaries noted that renewable fuels, including North Sky’s renewable natural gas (RNG) projects, have quietly benefited from enhanced incentives in the OBBB. Another positive indicator of sector sentiment is the pricing of Renewable Identification Numbers (RINs). RINs are credits central to the US EPA’s Renewable Fuel Standard program, ensuring compliance with mandates to blend renewable fuels—like ethanol, biodiesel and RNG—into transportation fuels. RINs act as the program’s “currency,” tracking production and use of renewable fuels to reduce greenhouse gas emissions and support domestic energy under laws like the 2005 Energy Policy Act and 2007 Energy Independence and Security Act. RINs remain attached to the fuel until the renewable fuel is blended with gasoline or diesel, after which the RINs become tradable commodities with fluctuating prices, valid for the generation year plus one (with limited carryover). The chart below shows RIN values remaining stable during the past two years despite political shifts.

RIN Prices 2024-2025

Source: Environmental Protection Agency

Portfolio Updates. North Sky infrastructure ended the year on a high note with four transactions during December. First, our battery storage joint venture (Orenda) closed an interconnection deposit loan facility, providing both an interim exit and substantial reinvestment capital to continue growing that portfolio. Second, our solar development affiliate (Paddle) sold four additional projects in Maine for a substantial profit. Third, Infrastructure Investment Fund executed a Letter of Intent to acquire an equity stake in an existing portfolio of EV charging stations with attractive expansion opportunities. Fourth, Sustainable Infrastructure Fund IV executed a Letter of Intent with a new operating partner to develop and construct community solar facilities in Maryland and Minnesota.

Conclusion

In 2025, the “Solar Coaster” delivered a wild ride of policy shifts, geopolitical tensions, and volatile pricing, yet North Sky navigated the turbulence with resilience, discipline and opportunism—delivering strong performance and meaningful exits. Amid surging electricity demand from AI datacenters and EVs, breakthroughs in critical minerals recycling, and continued cost declines in batteries and renewables, the outlook for impact investing remains compelling. Solar and storage deployment accelerated, and secondary markets stayed robust despite improving primary exits. With a growing investment pipeline across the circular economy, energy transition, climate adaptation, smart grid, healthy living and other areas—and momentum building into 2026—North Sky is well-positioned to continue generating attractive risk-adjusted returns while driving measurable environmental and social impact.