Introduction

North Sky had a great start to 2023. Among our accomplishments:

- We completed two big exits for our sustainable infrastructure strategy (KDC Solar and Volney-Marcy transmission line)

- Added preeminent impact investor Stefan den Doelder to our impact secondaries team (Rotterdam)

- Congratulated Tom Jorgensen for being named “one of eight people who will shape sustainable private markets in 2023” by New Private Markets

- Bolstered our impact data collection, analysis and reporting technology and successfully navigated the Article 8 requirements under Europe’s Sustainable Finance Disclosure Rules for Clean Growth VI (“CG VI”)

- Enhanced our investment process by adding Lucy Fan to the Sustainable Infrastructure Fund IV (“SIF IV”) investment committee and Angie Wood to the CG VI investment committee

- Created a new ESG policy committee to bolster our ESG risk assessment and reporting procedures

- Successfully navigated the stormy Silicon Valley Bank waters

- ImpactAssets named North Sky to its IA 50 list, for the sixth consecutive year, which recognizes investment managers who demonstrate a commitment to generating positive social, environmental and financial impact.

Our secondaries team is benefiting from the intersection of several trends that are setting up for a buyer’s market in key impact sectors such as circular economy, sustainable food and climatech. We also are happy to report that pricing held steady in our impact secondaries niche, while pricing in the traditional secondaries market ticked up from 79.9% of 6/30/22 NAV to 82.9% of 9/30/22 NAV as those fund managers rushed to make up for previous quarters of lower activity. Average pricing for traditional secondaries from March 2017 through September 2022 (most recent data available from PEFOX) has been 89.0% of NAV. Pricing for our Clean Growth strategy has been well below that level (approx. 58%) due to our position in this impact marketplace, among other factors.

In a follow-up to our Q4 market commentary, our infrastructure team is reporting that there has been a sharp drop in lithium carbonate prices, which was welcome news for energy storage developers and investors like us. The team also set the stage for a win in our third infrastructure fund by assisting in the sale of a portfolio of community solar assets that will occur in installments over the next 18 months. The IRS and other federal agencies have been busy writing regulations to clarify how to qualify for the incentives in the Inflation Reduction Act (“IRA”). More on this below.

There was one other noteworthy occurrence in Q1, the horrific train derailment in East Palestine, OH (followed by others in Minnesota and North Dakota and elsewhere). These accidents caused immense damage to the people and the environment in those areas and remind us that we must keep striving to do better. We must upgrade our aging infrastructure—rail, bridges, highways, airports, seaports, energy production and distribution. We should also create new infrastructure such as recycling capabilities for EV batteries, solar panels and wind turbine blades and more efficient shipping methods such as hyperloops between major cities to reduce trucking and safe, quiet drones for last mile delivery to homes. We are moving into a new era and our infrastructure needs an upgrade. We hope you will join us as we do our part.

Market Update

Vast untapped impact secondaries market. Our impact secondaries strategy is focused on opportunities that have largely been overlooked, orphaned or misunderstood. We believe the impact secondaries market is vastly untapped, which provides pricing power and attractive entry points for buyers like us that have both capital and deep industry expertise.

The traditional secondaries market began in 1984 with a $6 million fund managed by VCFA but did not become part of the institutional investment vernacular until about 2003. It is a very mature marketplace today with over 400 active secondaries firms and $103 billion in transaction volume in 2022 (source: Secondaries Investor). We believe the impact secondaries market we created in 2013 will follow a similar relative path.

We did a little math to show that potential. Since 2007, traditional secondary funds accounted for about 3.7% of all private capital raised (Source: Pitchbook). In the same period, we believe dedicated impact secondary funds accounted for 0.1% of all impact capital raised ($422 million of $380 billion). That is quite a gap between the secondary dollars raised for the traditional market vs. the impact market. Based on fundraising data from Pitchbook, an average of $47 billion was raised by impact funds in each of the last four years. Extrapolating, that means $1.7 billion in impact secondaries funds should have been raised (3.7% of $47 billion) in 2022 for example but instead only about $100 million was raised. Furthermore, by our estimates, there is approximately $209 billion of potential market opportunity for impact secondary transactions. All of this indicates there is great potential to grow this strategy.

Global Impact Private Market Fund AUM ($ billions)

Source: Pitchbook

Source: Pitchbook

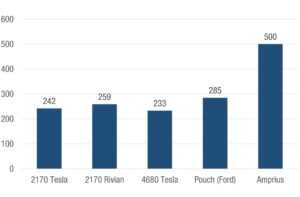

Battery breakthrough. One of our Clean Growth IV portfolio companies, Amprius (NYSE: AMPX), recently reported a tremendous battery breakthrough. Using proprietary silicon anodes, the company’s lithium-ion batteries deliver double the energy density compared to other common batteries such as those used in Tesla, Rivian and Ford EVs. This has important implications for future EVs and for electric powered drones and other aircraft. This allows customers to “either increase energy content in a battery pack without increasing weight, reduce weight in applications that target a fixed energy content, or combinations of both,” according to the Amprius press release.

Energy Density (Wh/kg)

Source: Bloomberg NEF

Exit activity. North Sky’s Infrastructure team had an active start to 2023. We closed on the sales of a high voltage transmission line in New York State (Volney-Marcy) and a 34 MW solar portfolio in New Jersey (KDC), resulting in a large cash distribution to investors in our second infrastructure fund in Q1. Additionally, one of our solar developer partners for our third fund closed on the sale of a 76 MW portfolio of community solar projects in Maine. We also continued to invest in the construction of our recent investments in renewable natural gas, energy storage and solar projects.

Policy update. On the policy front, the first quarter of 2023 saw continued rulemaking activity regarding the IRA. As a reminder, once federal spending legislation is passed, agencies such as the Internal Revenue Service, US Treasury, Department of Energy and Department of Labor must issue the “fine print” detailing how businesses can achieve the incentives in such legislation. In February, the federal government issued initial rules governing the issuance of an additional 10% Investment Tax Credit (“ITC”) for renewable energy projects in Qualified Low Income Communities. This 10% ITC is additive to the existing 30% ITC for certain renewable energy projects such as wind and solar facilities. Renewable energy developers and project owners had been awaiting this rulemaking, and it gives some clarity to 2023 project proformas.

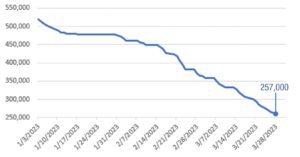

Lower lithium prices. In our last market commentary, we wrote about the demand for battery materials increasing almost 30% over the previous year, straining the market. Supply chain pressures resulted in production and delivery delays and significantly higher prices for battery components such as lithium carbonate. Wood Mackenzie reported that the US grid-scale segment installed only 848 MW of batteries in Q4, a decline from the previous two quarters of 1+ GW deployments in each.

However, the rapid rise in lithium carbonate prices observed in 2022 underwent a strong reversal in the Q1 of 2023. During the quarter, pricing dropped from over 500,000 RMB/ton to just over 250,000 RMB/ton today.

Lithium Carbonate (99.5% Battery Grade) Prices

Source: Shanghai Metals Market

Demand remains strong, but prices had been unsustainable for some time. Supply is finally coming on stream faster, a large portion from China, Australia and Chile. The turning point for lithium prices came late in 2022 as electric vehicle demand in China slowed sharply ahead of Beijing’s planned halt to subsidies for the $87 billion industry. With the increased supply, experts forecast the global market deficit of lithium will shrink from 76,000 metric tons in 2022 to 20,000 metric tons in 2023. Looking forward to 2025, experts expect lithium supply growth of 34% a year to outpace the demand growth rate of 25%.

While prices on battery precursors peaked in Q4, labor costs are expected to remain elevated. The IRA has driven higher labor costs, both by increasing demand for EPC companies across the renewables industry and by leaving EPC firms responsible for compliance with the Act’s apprenticeship and prevailing wage requirements.

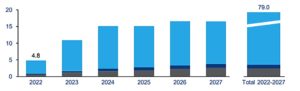

While the storage industry faced headwinds in 2022, the longer-term outlook remains strong, as illustrated below. North Sky’s infrastructure portfolio contains several battery storage projects, and we expect those assets to grow in 2023.

US Annual and Cumulative Battery Market Outlook (GW)

Source: Wood Mackenzie