introduction

The second quarter was jam-packed with activity and market conditions are very strong for both impact secondaries (due mostly to large PE investors needing to sell existing holdings to generate liquidity) and sustainable infrastructure (thanks to huge tailwinds from the ongoing transition to a renewable energy and EVs and the Inflation Reduction Act). Our secondaries team, investing on behalf of Clean Growth VI, completed its 7th investment during the quarter, which was a multi-asset continuation vehicle that we formed to acquire the carbon neutral-focused corporate venture capital portfolio of French energy giant Total. The portfolio consists of approximately 20 companies in North America and Europe. Our infrastructure team was honored to have its Victor Valley RNG project recognized as Wastewater Project of the Year by the Global Water Awards. One of our portfolio companies, Gradiant, was also named Desalination Company of the Year by the same group. Gradiant is held within Clean Growth IV and Clean Growth V, although those stakes were acquired at different times and via two different private equity firms. We also issued our 2023 Impact Report and welcomed intern Robel Zewdie, who is studying finance and math at the U of MN’s Carlson School of Management.

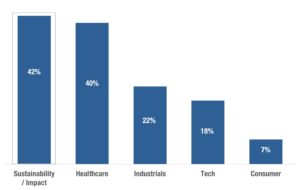

Further, a recent survey by Rede Partners showed very strong interest among institutional investors to make new commitments to Sustainability / Impact investments, particularly among European investors.

To Which Sectors Do You Plan to Increase Allocations for 2023?

European LPs

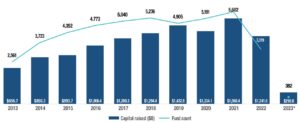

On the flip side of all that good news, fundraising across all private markets is down. According to Pitchbook, fundraising surged post-covid to $1.56 billion across 5,602 funds in 2021. But 2022 garnered only $1.24 billion across 3,319 funds. Q1 data shows 2023 is tracking well below 2022 with just $211 million raised across 382 funds (i.e., $844 million and 1,528 funds if annualized).

Private Capital Fundraising Activity

Source: PitchBook · Geography: Global

*As of March 31, 2023

On a related note, average fundraising time for private funds also seems to have increased, with many fund managers asking for extensions. Per RSM, top quartile fund managers are now taking an average of 19.8 months to reach a final closing.

Market Update

Buyer’s market for impact secondaries. Based on our market analysis, we believe there is approximately $100 billion of unrealized Net Asset Value (“NAV”) currently held by impact funds located in the USA, Canada, Europe, Israel, South Korea, Japan, Australia, New Zealand and other developed areas. This represents a significant buying opportunity. Further with (a) the IPO window nearly shut, (b) SPAC activity almost non-existent and (c) the M&A market diminished from recent peaks, liquidity for existing private markets investors has slowed to a trickle. That means many investors have turned to the secondaries market for near-term liquidity. We are among the beneficiaries of heightened secondaries deal flow and, since we have almost no direct competition in the impact niche, we expect the next several quarters to be an outstanding opportunity for buyers of impact secondaries.

While individual sales of LP interests in impact funds are still relatively small—often $5-20 million per transaction—the size has steadily grown since we launched our strategy 10 years ago. We attribute this to a maturing marketplace, a secular trend among institutional investors to increase their allocations to impact investments since 2012, the resultant need/desire to occasionally rebalance their portfolios to meet asset allocation targets (including impact assets) and the growing number of $500+ million funds that have entered the market since 2015.

We expect our typical bite size to increase in each of the next few years as the total impact assets held by institutional investors continues to accumulate and more of those assets reach the point where rebalancing and/or liquidity is needed/desired. While it is common for blocks of $100-200 million of private investments to trade hands in the traditional secondaries market, we do not expect that to be common within the impact secondaries market for a few more years. However, we can see it coming over the horizon. While it is anecdotal, we are sourcing $20-30 million impact secondaries opportunities with increasing frequency lately and are currently reviewing one $50+ million opportunity. We expect those numbers to grow over the next two years. In the meantime, we continue to build out our network of GPs, LPs, brokers, bankers, lawyers and accountants to keep growing our proprietary deal sourcing capabilities in this important investment sector.

We also want to touch upon GP-led transactions where there is a greater ability to invest larger sums of capital in continuation vehicles. We are seeing a range of opportunities from $10-30 million vehicles where we might be the sole investor to $100+ million syndicated transactions (most often in healthcare or circular economy sectors) where we may assist in diligencing the opportunity, pricing the deal and building out the syndicate. Companies that benefit from the Inflation Reduction Act such as energy, transportation, distribution and circular economy are of heightened interest today. Specifically, we have seen several large single asset continuation vehicles and co-investment opportunities targeting the waste/recycling industry over the past year. Some of these opportunities appear to be a good fit for CG VI to participate as a member of the syndicate and might also result in co-investment opportunities for our LPs.

Leverage in secondary funds. It is well known that traditional secondary funds have historically been heavy users of leverage, most of which has a floating interest rate. From 2008-22, thanks to unusually low interest rates, this generated eye popping IRRs in some cases. In others it provided the return boost needed to get to a minimum underwriting hurdle and therefore justify paying a high price with minimal to no discount to NAV. We estimate the cost of leverage has increased by 400-500 basis points in the past year for most secondary funds. Notably, the Prime Rate was just 3.5% in March 2022 but rose to 8.25% by May 2023. Secondaries funds that relied on cheap leverage now find themselves in hostile territory. We expect many such funds will generate underwhelming investment returns for their 2019-2023 vintage year funds because exits are occurring later than originally expected and their debt is more expensive and will be outstanding longer than anticipated. At North Sky, our impact secondary strategy has never used long-term leverage!

Parting thought. Many Investors are still tiptoeing into impact investments, especially US and Canadian investors. An impact secondaries strategy allows such investors to reach back in time to earlier vintage years to add diversification and to more quickly and efficiently fill out their impact allocations. The typical reverse J-curve of secondaries funds can be another benefit for investors making commitments to new impact funds (i.e., the secondaries fund softens the J-curve created by the commitments to new funds).

Following a busy first quarter of transaction activity, North Sky’s Infrastructure team focused on creating value in our existing funds in the second quarter, along with monitoring several positive developments on the policy front. Our Victor Valley renewable natural gas (“RNG”) project, mentioned above, is producing its highest gas volumes since construction was completed in 2022, and began selling RNG to Toyota in May, for the automaker to use as a feedstock for renewable hydrogen vehicles. Our Rhode Island Bioenergy Facility asset, a food waste processing facility that is undergoing a conversion from producing electricity to producing RNG, continues to meet its construction schedule and is expected to begin producing RNG in the third quarter of this year. Both investments are held in our third infrastructure fund (IIF).

IIF’s battery storage partner Orenda will be bringing 60 megawatt-hours of standalone battery storage capacity to the New York market in the third quarter of 2023. Verdonck Partners is advising on the transaction. These first four projects, part of a larger 337 megawatt-hour portfolio, will commence commercial operations before the summer 2024 season, and will deliver resiliency and peak demand management capabilities to downstate New York. This is a region that desperately needs these battery resources due to pending peaker plant retirements and electrification trends. The projects benefit from recent federal guidance on the Investment Tax Credit bonus categories and direct transfer of those credits. In addition to federal support, the projects benefit from NY State’s commitment to a nation-leading target of 6 gigawatts of storage by 2030, as part of New York’s Energy Storage Roadmap 2.0.

IIF’s joint venture with Paddle Energy, a solar and storage development company incubated by North Sky, continued to grow its project pipeline and is focused on the fast-growing community solar market segment. Its greenfield development pipeline stands at 30MW as of the end of the second quarter, with an emphasis on Maine’s Net Energy Billing program. Further, solar project development activity is expanding into Maryland, another state with favorable community solar regulations.

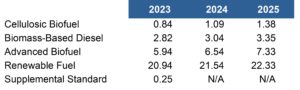

Policy Update. On the policy front, on June 21, the U.S. Environmental Protection Agency (“EPA”) released its Renewable Fuel Standard (“RFS”) volume targets for 2023-5, plus important modifications that strengthen and expand the RFS program. The final volumes are as follows:

Volume Targets (billions RINs)

a One RIN is equivalent to one ethanol-equivalent gallon of renewable fuel

b BBD is given in billion gallons

Given the EPA’s history of releasing volume targets just in time (or retroactively in the case of 2020-2022), this 3-year forward guidance provides some welcome clarity and market certainty. Further the EPA increased projections for CNG/LNG production for the period, using a 25% growth rate reflective of recent strong investments in RNG projects. Other important program modifications will benefit the industry overall and our IIF portfolio specifically. Most notably, the EPA provided guidance for the apportionment of RINs when feedstocks that qualify for multiple RIN categories are converted to biogas simultaneously in an anaerobic digester. This allows for co-digestion of multiple feedstocks such as wastewater sludge and food waste, which is what our SoCal Biomethane project is doing. We have similar digester projects in our deal pipeline that may be applicable to IIF or our new fund, SIF IV.

Over the past quarter, the IRS has released key guidance on the ITC bonuses and the new transferability provisions.

- First, the IRS provided details on the energy community bonus credit that expanded the original interpretation of energy communities. IIF portfolio projects are likely to be “safeharbored” for the energy community bonus which applies to (i) sites that are already viewed as a brownfield under federal and state programs and (ii) small projects under 5 MWACwhere a Phase I environmental site assessment did not come back “clean.”

- Second, the IRS provided details on how to determine whether projects qualify for the bonus tax credit for using enough domestic content. The analysis is more complicated than expected, and IIF partners are still verifying our bonus eligibility.

- Third, the IRS provided guidance that allows tax credit transfers to take place. Prior to the Inflation Reduction Act, it was illegal to buy and sell federal tax credits generated by renewable energy projects. Instead, developers entered into complicated partnerships with companies (often banks) that had sufficient tax liability to monetize the credits most efficiently. The transferability provision allows for a larger universe of taxpayers to take advantage of the credits and allows developers to avoid the complicated tax equity structures previously required. It is expected that the market for tax credits will double or triple because of these new provisions.

Conclusion

We are playing an active role in the global transition to a more sustainable future. That transition appears to be a multi-decade investment opportunity in major areas like energy, transportation, food, water, sanitation and healthcare. Our flagship strategies are differentiated, authentic and impactful. The Inflation Reduction Act has put a spring in our step, summer is here and we feel like we are walking on sunshine. We hope you will join us if you haven’t already. To learn more, please contact Erika Gucfa or Gretchen Postula.

We also wish our American readers a happy Independence Day and a safe holiday weekend!