Arete is an ancient Greek concept meaning “excellence” or “effectiveness,” embodying the ability to perform one’s function well. To us at North Sky, it means pursuing constant improvement and striving to set the gold standard for impact investment firms. We are always happy warriors, but particularly so in these times of rapid technological advancements, major public policy shifts and market volatility.

We had another great quarter in Q1. Despite geopolitical and market turbulence, we chalked up numerous wins for both our impact secondary and sustainable infrastructure strategies. Specifically, we held a second closing on Clean Growth VII, bringing us to more than 2/3 of our fundraising target. Our fundraising progress was made possible by a terrific group of long-standing LPs, as well as important newcomers from across the globe. Thank you!

During the quarter, we were named to the 2026 ImpactAssets 50 list as an Emeritus Manager, spoke at the Responsible Investment Forum in NYC and Confluence Philanthropy’s 16th Annual Practitioners Gathering in Asheville and attended the Higher Education Climate Leadership Summit in Chicago and Infocast (Solar + Wind Finance & Investment Summit) in Phoenix. North Sky also added Sam Weintraub as an Analyst on our impact secondary team—welcome Sam! Seven of our portfolio companies were named to the Global Cleantech 100 list.

North Sky Portfolio Companies Named to the 2026 Global Cleantech 100 List

Finally, our impact secondary team made exciting new investments that brought great companies into the fold like Good Culture, Sustainable Intelligence, Chasm and Handshake: the career network for the AI economy, and our sustainable infra team commissioned two new energy storage projects in New York and started a series of distributed generation solar projects in Pennsylvania, which is an attractive new market for us.

Contributing to our investment success was the uncertainty caused by geopolitical/market jitters, which propelled selling LPs and liquidity-constrained GPs into the arms of our secondaries team and anxious early-stage developers toward our infra team. We also continued to benefit from the $2.3 trillion infrastructure investment cycle—the largest in US history. This cycle, which is expected to span 2020-2035, is being driven by the convergence of AI compute demand, domestic semiconductor reshoring under the CHIPS and Science Act, the Inflation Reduction Act and the Bipartisan Infrastructure Law (also known as the Infrastructure Investment and Jobs Act).

Today, we are seeing important advancements in the following sectors:

- Climatech / Technology—a steady march of improvements across smart grid/homes, cybersecurity, solar panel/inverter efficiency, water tech, AI-in-everything and battery chemistry, which is now capable of charging an EV in three minutes

- Energy—e.g., solar panel improvements plus progress on small module reactors and nuclear fusion

- Mobility—e.g., the first Cybercab was built in February

- Healthier food and food supply chain—e.g., poultry and pork processing and food traceability standards recently rose

- Healthcare—e.g., several cancer and immunotherapy breakthroughs, including for treatment of breast and pancreatic cancers

- Medtech—e.g., surgical robots and AI-powered imaging for stroke diagnostics

- Education—mostly thanks to AI and moves toward personalized learning

During the quarter, we also witnessed several macro trends:

- Price increases globally for certain commodities such as oil, natural gas (especially in Europe and Asia), gold, silver and wheat.

- Continued rising energy demand thanks to AI, data centers, EVs, heat pumps and industrial reshoring of manufacturing operations (note also the announced restarts of old nuclear power plants in Japan, Iowa, Michigan and Pennsylvania).

- Big regulatory changes in the USA, including:

-

-

- EPA rescinded its 2009 Greenhouse Gas Endangerment Finding, which served as a prerequisite for regulating CO2 emissions from motor vehicles and encouraged the transition to EVs.

- FDA launched the Adverse Event Monitoring System (AEMS) to replace seven outdated system from the 1990s meant to track adverse events (such as death, paralysis, brain injury, etc.) across vaccines, drugs, medical devices, cosmetics, foods, tobacco and veterinary items. Previously, less than 1% of vaccine adverse events were being properly captured, according to a Harvard Pilgrim Health Care study! The FDA is also reviewing food additives and coloring.

- HHS announced a reset of dietary guidelines for Americans (aka the “food pyramid”), marking the most significant change to national nutrition policy in decades. The goal is to restore scientific integrity, accountability and common sense to federal health guidance and to “prioritize whole, nutrient-dense foods—protein, dairy, vegetables, fruits, healthy fats and whole grains—and dramatically reduce highly processed foods.”

- USDA created new standards for meat, poultry and egg products to be labeled a “Product of the USA.” To qualify animals must be born, raised, harvested and processed entirely within the USA. Previously, animals essentially could be born and raised outside of the USA but processed within the USA and still claim to be a US product. The USDA also approved new verification standards to back up marketing claims such as grass-fed, antibiotic-free and cage-free.

- A new direct-to-consumer drug portal aimed at affordability also launched.

-

Impact of the above trends on CG VI portfolio companies:

- PivotBio is poised to benefit from the increase in natural gas prices because its products are considered a substitute for fertilizer, which has skyrocketed in price because it is typically derived from natural gas.

- Crusoe calls itself the AI factory company and provides renewable-powered AI infrastructure. During 2025, Crusoe partnered with Redwood Materials to create the world’s largest second-life battery deployment, using solar power and repurposed EV batteries to power off-grid AI data centers. This strategic initiative delivers a scalable, clean energy solution to meet the growing power demands of AI. In early 2026, this effort was expanded to bring total compute capacity to nearly 7x the original deployment. The modular nature of both Crusoe’s data centers and Redwood’s storage systems allows for rapid deployment (in months rather than typically years-long construction builds), paving the way for fast, responsible AI infrastructure growth. Furthermore, Crusoe also has a partnership with Form Energy (which is in CG V) to deploy 12 GWh of multi-day energy storage systems to support the power needs of AI data centers starting in 2027. The deployment will utilize Form Energy’s iron-air battery systems, which in essence use iron’s oxidation process (commonly referred to as “rusting”) to release electrons to power data centers. The oxidation process is reversible so the batteries store energy when electricity is delivered into the system, returning the iron to its previous “non-rusted” state.

- CG VI has smartly played into the health/healthy food trend via secondary investments that provided exposure to companies like Aloha, Purely Elizabeth, Good Culture, Western Smokehouse and CR Fitness (a large franchisee of Crunch Fitness gyms).

- Medable may tangentially benefit from policy changes relating to vaccine and drug safety.

We are, of course, also closely following AI trends, fears within the private credit market, the IPO calendar, the war in Iran and geopolitical matters in Venezuela, Cuba, Russia and China, among other major variables in today’s market.

All of this is to say we are living in a time of unprecedented change—technological, economic, political, etc. Those changes are creating new investment opportunities, and we are here for it!

Market Update

Secondary Market Volume. Each year in Q1, investment banks publish secondary market volume surveys. They provide a useful opportunity to step back, assess where the broader market is heading and evaluate which trends are relevant—and which are not—for impact secondaries.

Across the 2025 reports, several consistent themes emerged, with clear implications for our strategy:

- Secondary volume reached a new high, with approximately $225 billion transacted, split 54% LP-led and 46% GP-led.

- Dry powder is constrained. Greenhill estimates that dry powder compared to LTM transaction volume in the secondary market is a mere 1.4x ratio, down from 1.6x in 2024 and 2.3x in 2023.

- Market share is consolidating. PJT reports that the top 10 buyers accounted for 53% of total volume.

- Transaction sizes continue to scale. Jefferies identified nine LP-led transactions over $2 billion, with average deal size increasing to $450 million.

- Continuation vehicles (CVs) are growing in size and frequency. Morgan Stanley notes 20 single-asset and 13 multi-asset CVs exceeding $1 billion, while CVs continue to represent ~15% of sponsor backed exit volume. Notably, 83% of the top 100 sponsors have completed at least one CV, and 63% more than one.

- Pricing dispersion remains pronounced in venture and growth secondaries. PJT shows pricing varies widely depending on the perceived quality and stage of the portfolio, while Greenhill reports buyers are reluctant to underwrite unfamiliar or niche strategies—often resulting in bid-ask spreads exceeding 20% of NAV.

While capital and transaction volume are increasingly concentrated among the largest secondary sponsors, impact secondaries remain fragmented and structurally underserved. Impact deal sizes are well below industry averages, and venture/growth portfolios of impact companies are largely ignored by the big traditional secondary funds—despite attractive fundamentals.

This fragmentation creates opportunity for specialists like us. Our global impact network—which has been growing for over two decades—combined with a deep secondary track record positions us to underwrite complexity, bridge expectation gaps and capitalize on inefficiencies that generalist platforms often overlook. We continue to operate with very limited competition, at a time when demand for liquidity solutions far exceeds available secondary capital.

Clean Growth VII Activation. Clean Growth VII made its first investment this quarter (a GP-led investment involving a 2018 vintage fund). The deal was sourced through our long-standing relationship with an experienced GP focused on energy, food, water and waste management. The key portfolio driver is UK-headquartered Carbon Clean, which supplies cost-effective, industrial carbon capture solutions within the data center, cement, steel and energy sectors and whose customers include Chevron, Cemex, Samsung and Kanoo Energy. We have a terrific pipeline of new investment opportunities and are lining up other investments for Q2, including GP- and LP-led opportunities with attractive discounts. We believe this is one of the most compelling investment environments in our history, due largely to (1) recent regulatory and policy changes in the USA and other G20 countries, (2) advancements in technology and (3) the maturation and broadening of the impact investing universe.

Portfolio Updates. Clean Growth VI is wrapping up its final investments. Q1 revealed the culmination of significant efforts over the last nine months to source, analyze and negotiate attractive entry points for five investments, which span climatech, circular economy, healthy food and job creation/pairing for college graduates. CG VI’s final two investments were also approved during the quarter—in the areas of water and healthcare—and are expected to close in Q2.

CG III, IV and V are in harvesting mode, and we are striving to make final distributions from those funds by yearend 2026, 2027 and 2029, respectively.

Strong Deal Momentum Continues. Our previous Market Commentaries discussed the growing demand for power globally and that a combination of new solar and storage projects has been responsible for meeting most of that demand. For example, solar accounted for 54% of the new capacity additions in the US in 2025. The dealmaking required to support this growth continues as well.

The North Sky Infrastructure team attended the annual Infocast (Solar + Wind Finance & Investment Summit) in Phoenix, along with over 3,000 other participants. Our meetings with development partners, project lenders, tax credit buyers, insurers and fellow investors affirmed our belief that we are operating in a growing market with underlying policy stability. Other key topics we discussed at Infocast include the challenge of navigating supply chains to satisfy domestic content rules for new projects and the growing market for tax credit insurance—which helps small and medium sized developers access the tax credit market.

Renewable Natural Gas. The RNG industry, globally and domestically, continued its steady expansion through Q1. A North Carolina biogas facility earned a BBB rating from S&P for a $110 million bond issue, which we believe is the first investment-grade RNG project finance bond rating not otherwise issued under municipal or special green bond indentures. In February, the Treasury issued long awaited guidance for claiming RNG 45(z) federal tax credits, which were extended as part of the One Big Beautiful Bill. However most significantly for North Sky, our SoCal Biomethane RNG project became the first operating project to receive a long-term gas offtake agreement under California SB 1440, an important milestone for both the project and the California RNG market. Read more here.

Portfolio Updates. North Sky’s New York battery storage portfolio continues to advance, which is owned by both SIF III (aka IIF) and SIF IV. We secured additional demand load management awards from the local utility, which enhance those projects’ revenue projections. Battery prices are favorable primarily due to the cancellation of the IEEPA tariffs and despite ongoing fluctuations in the lithium carbon commodity price. In Q1, we launched a process to sell the next vintage of projects. We also await the finalization of the marginal cost of service rules, which could enhance revenue projections by up to 25% for certain aspects of our battery portfolio. Nationally, domestic battery storage project deployments are expected to require over $25 billion in capital in 2026 (per the SEIA), signaling continued sector growth and opportunity for us.

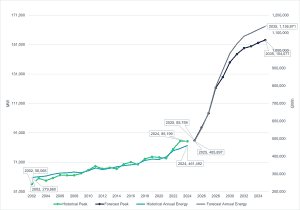

Texas is expected to overtake California in 2026 as the state with the largest solar capacity. Texas grid operator, ERCOT, anticipates significant load growth driven by AI and data centers, industrial electrification, hydrogen production and EV adoption (see chart below). ERCOT’s load queue jumped almost 300% in 2025, indicating ERCOT will need to substantially grow generation and transmission resources to meet new demand. SIF IV owns nearly 1 GW of ERCOT storage development assets, which are poised to benefit from this demand.

Annual Energy vs Peak Demand ERCOT Based on ERCOT Adjusted Forecast

Source: ERCOT

Conclusion

In a quarter defined by rapid technological progress, significant policy resets and persistent market volatility, North Sky continued to set the standard in the impact marketplace. Our ability to deliver strong results for both our strategies amid these conditions reflects the power of our specialized approach, deep industry relationships and unwavering focus on long-term value creation.

The convergence of structural tailwinds—surging energy demand from AI and data centers, maturing climate technologies, policy shifts that reward pragmatism and domestic supply chains, and an undercapitalized impact secondaries market—has created one of the most compelling investment environments we have seen. We are capitalizing on this moment: deploying capital into high-conviction GP- and LP-led secondaries at attractive terms and scaling our RNG, energy storage and solar portfolios.

Looking ahead, we expect our differentiated network, rigorous underwriting and proactive portfolio management skills will continue to provide a meaningful edge in a fragmented and opportunity-rich landscape. We will continue to strive for excellence in every investment, every partnership and every outcome—because true Arete is forged during transformative times.