Introduction

The first half of the year has been a whirlwind of activity. Investment opportunities continue to be very strong for both our strategies (sustainable infrastructure and impact secondaries). Our infrastructure team was named by Preqin as one of the Most Consistent Infrastructure Performers (third best in the manager universe). Further, our infrastructure team is making the first investment for Sustainable Infrastructure Fund IV—a series of battery energy storage projects in the NYC area that will provide peak load shaving services to the grid during the summer months and demand response power year-round. SIF IV targets three main sectors: environmental infrastructure, clean power and grid enhancements. The team has an active pipeline of investment opportunities that includes renewable natural gas, community solar, green hydrogen, energy storage, geothermal, microgrids, lithium carbonate processing, various waste-to-value projects and carbon sequestration.

Our impact secondaries team has also been busy. On June 30, we held the final closing of Clean Growth VI at $252mm (press release), and the team has invested approximately $145mm of that total. For CG VI, we are building a diversified portfolio across climatech/cleantech, circular economy, water, healthy living, education and related areas. Illustrative examples from the CG VI portfolio include Power Plus Communications, CarbonFree, KeyDHT and Hyland’s Naturals.

CG VI has already had several early liquidity events, which has returned 27% of the capital invested to date. We have recycled the proceeds from a portion of these early liquidity events and will make the first distribution to CG VI LPs later this month.

We also published our 2024 Impact Report in Q2. Find it at the top of our website here.

Market Update

Size of Impact Secondaries Market. When we launched the world’s first impact secondaries fund in 2013, this investment niche was a blank canvas. It was also small. The initial pond we were fishing in included about 300 funds raised mostly from 2005-8 with a combined Net Asset Value of a few billion dollars. Nearly all of those were early stage venture funds and almost all were limping severely still from the great financial crisis. A lot has changed since then.

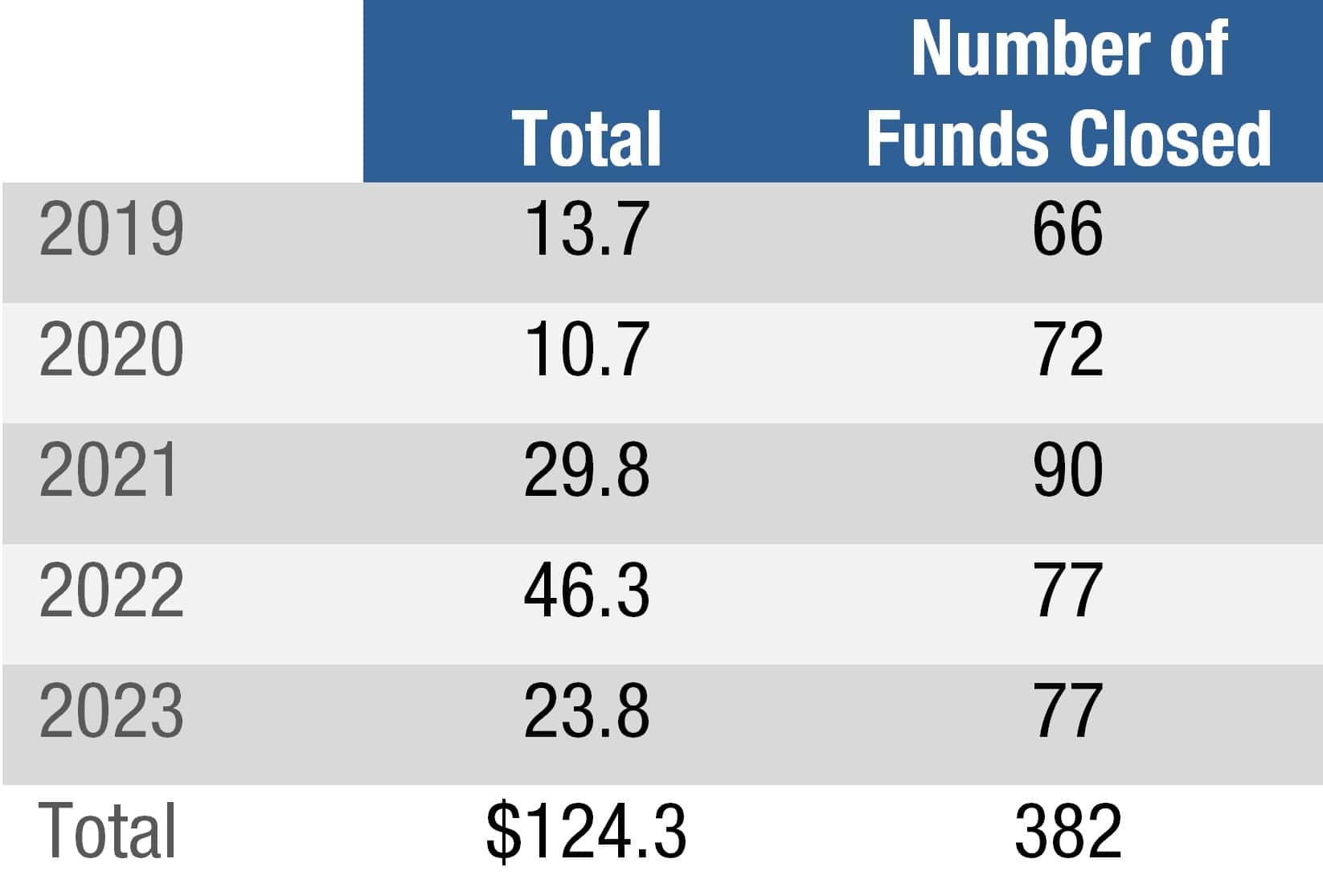

Today, that pond has grown tremendously in size and scope and is no longer limited to impact/cleantech funds. First, the scope has expanded to mirror all the investment strategies of the traditional private equity market, to wit: seed, early stage and late stage venture capital, growth equity, private credit, mezzanine, buyout and infrastructure funds. Second, the amount of impact dedicated capital raised has grown tremendously in recent years. As noted in the New Private Markets table below, impact managers have raised $124 billion across 382 funds in the last five years.

Year-on-Year Fundraising ($bn) 2019-2023

The advent of GP-led solutions further expanded this investment universe to include impact companies that are held in funds that were never intended to employ an impact/ESG strategy. Many of these companies fall in the climatech/cleantech and circular economy themes which have “gone mainstream” over the last decade. In recent years, we have seen many traditional private equity firms move at least part of their investment capital in the direction of impact. Some of these moves were unintentional but many were purposeful as big firms like TPG, Bain, KKR and others could see the inherent benefits of resource efficiency, waste reduction, renewable power and related trends for their own portfolio companies. Some were quicker to the party than others, but a broad cross-section of the PE world is now adopting ESG policies in one form or another—and expanding the universe of actionable targets for North Sky as they do. As a secondary investor, we can sift through opportunities within these “traditional” PE funds to find investments that fit squarely within our key impact themes: cleantech/climatech, circular economy, sustainable food, healthy living, education, etc. As a point of reference, approximately 75% of our qualified impact deal flow comes from impact dedicated managers with the balance coming from traditional PE managers. Looking ahead, we expect this balance will become more equal over time.

Market Updates. Policy momentum continued to build for sustainable infrastructure throughout the United States. Notably for Fund III’s portfolio, New York State updated its Energy Storage Roadmap to expand its battery storage deployment goals, which enhances the opportunity set for our partnership with Orenda. In the RNG sector, Southern California Gas sent its first requests to the California utility commission to “rate-base” renewable natural gas projects under California Senate Bill 1440, which requires California gas utilities to procure RNG. Our Victor Valley Wastewater project is expected to benefit from future gas offtake within the 1440 program.

At the federal level, the US Treasury continued a flurry of “rulemaking” activities to finalize the requirements for renewable energy projects to qualify for various Inflation Reduction Act (IRA) incentives. Notably for the North Sky portfolio, final rules were issued for tax credit transferability and prevailing wage and registered apprenticeship, providing clarity for how developers and builders will qualify for, and monetize, IRA tax credits. Importantly, our projects qualified under the initial rules, as well as the final rules.

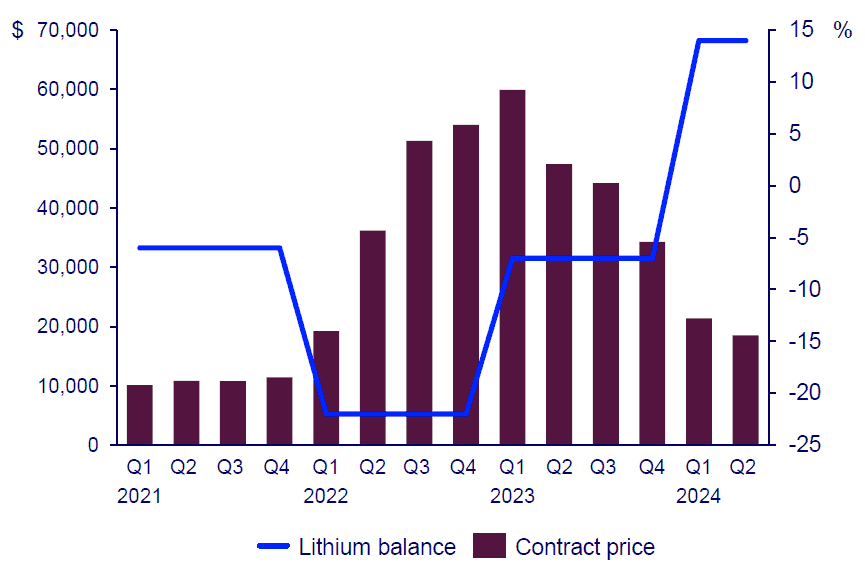

In our Q1 commentary, we discussed the growth in energy storage procurement goals. In this commentary we turn to the supply-side and capital costs of building those projects. The continuing price decline of lithium carbonate, the primary raw material in energy storage systems (ESS), has had significant impact on overall capital costs for storage. In 2023, the ESS battery cell market went from a deficit to a surplus as additional supply came online. Together with falling raw material prices, the price of an ESS lithium iron phosphate battery cell plummeted by more than 30% in 2023.

Price of battery-grade lithium carbonate ($/t real) versus annual lithium balance (%)

Source: Wood Mackenzie

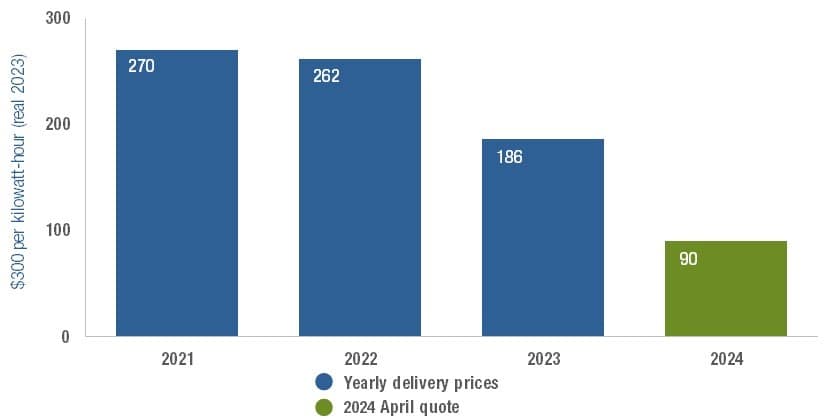

At the ESS level, the price decline is even more dramatic, with Chinese battery storage systems down 45% in Q1’24 compared to Q1’23. These factors enable the storage and solar-plus-storage developers that North Sky invests in to capture higher values for their project portfolios.

Chinese Battery Storage System Prices are Dropping Non-Linearly

Quoted China energy storage system prices more than halve in 2024

Source: BloombergNEF participants at the 12th Energy Storage International Conference and Expo (ESIE)

Recently in the RNG sector, the Canadian utility FortisBC became the first North American gas company to automatically designate a portion of their customers’ supply as RNG. This is analogous to many electric utilities increasingly designating a portion of the power sold to customers as “renewable.” This is an important trend we are following, where renewable fuels are increasingly used beyond just the transportation sector. This trend is consistent with the above-mentioned Southern California Gas request to the California utility commission.

Portfolio Updates. In Q1, we wrote about a setback for community solar gardens (CSGs) in California; however elsewhere CSGs continue to expand, including in regions where North Sky is actively investing. Today, 19 states plus Washington, D.C., have formal CSG policies, and the Solar Energy Industries Association expects the U.S. CSG market will add more than 6.6 gigawatts of new capacity this year. North Sky’s solar development platform, Paddle Energy, has continued to focus on community solar adding nine new projects in Q2, including rooftop, brownfield and solar plus battery storage sites. This brings the total Paddle Energy pipeline to 34 megawatts. Further, Paddle signed a Letter of Intent with a large aggregator of solar projects to sell its initial development projects at a large profit, consistent with its business plan.

Additionally, our ESS joint venture with Orenda has added 35 megawatts of development pipeline which correlates with the growth of the New York State storage market. Our Rhode Island Bioenergy project continues to ramp up following its commissioning in December 2023, setting new highs for RNG volume in Q2.

In a pleasant surprise for Fund II, three 20 megawatt solar development projects that had been sold to a large independent power producer were sold back to Fund II at favorable pricing. These projects are located in New York and may lead to additional gains that can be earned by that fund given a recent announcement by New York energy authorities that additional renewable energy procurements are likely in Q3.

Policy Update. Watch for our next Policy Update to be released later this month. To view our prior Policy Updates, they are in the research section of our website here.

Conclusion

We have reached the mid-point of the year. As we look ahead, we are expecting (a) an increase in private equity exit activity (which would be good for our existing funds CG III, IV and V in particular) and (b) significant new investment activity across our recent funds, including CG VI and SIF IV. We are cognizant that this is a Presidential election year in the USA and are tracking any major potential policy changes that November may bring, especially to our sustainable infrastructure strategy which is US-centric. We are also tracking public market activity, central bank prognostications, interest rates, tariffs, trade activity, AI’s impact on global power demand, European election outcomes, public policy changes and all the other myriad data that influence our two investment strategies.

We wish our American friends a belated Happy Independence Day and wish everyone a wonderful summer/holiday season.