Introduction

We have now passed the halfway point of 2025, and so much has already happened that it is hard to keep up. Some good, some bad, some neutral—and of course all subject to your personal viewpoint. But we view the glass as half full. Change begets opportunity.

We asked Grok for the best word to capture the experience of living through times of great political, technological and macroeconomic change. Grok responded with “whiplash,” which certainly captures today’s dizzying, wide-reaching, abrupt shifts. While we have written many times over the last 20 years that the rate of technological change is accelerating, we have not experienced a quarter where so much changed so fast. That’s not an ideal environment in which to write a quarterly market commentary, but we are undaunted!

We are living in a period of intense and rapid change that affects how we live, invest and plan for the future. Below is an illustrative list of recent major changes:

- Significant U.S. Policy Changes. President Trump’s second term began in January, resulting in policy shifts regarding trade, energy, technology, immigration and defense spending worldwide. Many of Trump’s priorities have been codified by the One Big Beautiful Bill Act (the “OBBB”), which, like many previous federal budgets, impacts the solar, wind and other renewable energy sectors.

- Tariffs and Trade Talks. On February 1, Trump imposed tariffs on imports from Mexico, Canada and China. On April 2, Trump announced a 10% baseline tariff on imports from all countries, as well as higher rates for dozens of nations that run trade surpluses with the U.S. Chaos ensues. As of early July, the U.S. has signed major trade deals with China, the UK and Vietnam and trade negotiations were still ongoing with the EU, India, Japan, Mexico and Canada, among others.

- Stock Market Volatility. The S&P 500 hit an all-time high closing price of 6,144 on February 19, 2025. The S&P 500 dropped 12% from April 2 (big tariff announcement) to April 8—and down 19% from its February 19 peak. As trade negotiations progressed, the U.S. stock market began to recover, with the S&P 500 climbing steadily to a new all-time high of 6,279 on July 3.

- U.S. GDP. GDP grew 2.4% in Q4 but contracted in Q1 (-0.5%). The contraction may have been due to a spike in imports as businesses tried to get ahead of tariffs (i.e., imports reduce the results of the GDP formula).

- Artificial Intelligence. Artificial Intelligence is rapidly changing how we search the internet, perform routine tasks and do business. AI is also increasing power demands worldwide, spurring construction of new energy generation and data centers worldwide.

- Political Leadership Changes. In addition to a new U.S. President, there have been major leadership changes during the last year in Australia, Canada, Japan, Mexico, Netherlands, South Korea and the UK plus nearly 20 other countries. And a new Pope in Vatican City.

- War/Conflict. Hostilities continue in Ukraine/Russia and Israel/Gaza. Brief conflicts between Israel/US/Iran and India/Pakistan quickly receded. Rwanda/DRC signed a peace agreement, ending a 30-year war.

- National Debt. The U.S. national debt was $26 trillion five years ago. It rose 42% since then to $37 trillion and is still rising. Annual interest payments exceed $1 trillion.

- Trust in media, politicians, central banks, insurance companies, pharmaceutical companies, the Food and Drug Administration, the World Health Organization and other institutions has cratered over the last few years.

While change can feel uncomfortable, many changes listed above provide the backdrop for new investment prospects. Cutting through the fog, we note the S&P 500 is up over 5% and the 10-year U.S. Treasury yield is down 20 bps year to date; the manufacturing cost of solar panels and large batteries continues to decline thanks to economies of scale; gas turbines are in short supply; nuclear power still takes a decade or more to build a new plant in the West; and the demand for electricity continues to grow worldwide due to trends in data centers/AI, EVs, demographics and other factors. We are long-standing impact investors, and we are using our experience, our networks and our knowledge to adapt to the noise and commotion. There is tremendous opportunity for impact investors with dry powder, a clear vision and a little intestinal fortitude.

Our infrastructure team is seeing opportunities in energy storage, community solar, data center-driven power demand and renewable fuels. Some of that opportunity involves partnering with developers that need liquidity to ensure their projects conform to post-OBBB requirements. Since 2010, this team has invested through nearly every permutation of political parties in control of the White House, Congress and local governments, sometimes with even shorter time horizons to capture incentives than what appear in the OBBB. Also, the infra team held a final close on SIF IV on June 30 and began seeking co-investment capital to invest alongside the fund. We hope you will join us in that capacity.

Our secondaries team has been inundated with GP-led and LP-led deal flow recently. Part of this surge is due to uncertainty about climate policy in the USA but most of it stems from investors pivoting to us to provide them with much needed liquidity across the entire breadth of our coverage sectors. Many of these sellers point to the lack of private equity exits over the last five years but that may be about to change.

Market Update

SIF IV Closed. As mentioned above, we closed SIF IV to new investors on June 30 and the fund is off to a strong start. SIF IV continues our long-standing investment strategy and is targeting mid-teens net IRRs. The first two investments are complete – energy storage in NY and a joint venture developing community solar projects in several Northeastern states along with energy storage projects in Texas. Looking beyond these projects, there are several additional near-term investment opportunities in the pipeline across key focus areas of RNG, community solar and energy storage. The portfolio is already valued above cost.

One Big Beautiful Bill. Our infrastructure team welcomed the final passage of the OBBB on July 4. Since the U.S. House Ways and Means Committee released its initial draft on May 12, energy developers had paused long-term planning, awaiting the final provisions. Failure to pass a budget would have resulted in further delays in strategic planning, as well as the possibility of another government debt-ceiling crisis and shutdown. While the final budget pulls back deadlines to complete certain kinds of projects, particularly wind and solar, it leaves the overall federal incentive architecture intact.

Both sides of the political aisle have sought to maximize the perceived magnitude of the changes in this budget, but here are a few things to consider:

- The level of federal support for renewables (30-50% Investment Tax Credit depending on domestic content and brownfield “adders”) and the tax credit transferability provisions in the Inflation Reduction Act remain unchanged.

- As we have previously written, and update below, the renewable energy landscape has evolved since the 2022 Inflation Reduction Act, driven by:

- surging power demand from data centers and electric vehicle adoption,

- onshoring of solar panel and module supply, and

- supply constraints and long lead times for coal, natural gas and nuclear energy, limiting their ability to meet near-term power demand growth.

- A reassessment of the timing and component requirements for renewable projects to qualify for incentives, alongside a changing landscape, should not be considered categorically hostile from a policy perspective.

The likely effects of the OBBB’s language will increase demand for domestic solar equipment and components and accelerate those purchase orders to qualify projects ahead of new deadlines. These outcomes are consistent with analysis and forecasts in previous North Sky policy updates. Specific revisions of previous law related to renewables include:

- Placed in service deadline of December 31, 2027, for wind and solar projects to receive tax credits, with this deadline extended for projects that “safe harbor” their “start of construction” prior to July 4, 2026.

- Expansion of Foreign Entity of Concern (“FEOC”) language to disqualify projects from receiving tax credits if those projects are owned, influenced or receive “material assistance” by entities in China, Russia, Iran or North Korea. Projects that safe harbor their start of construction prior to December 31, 2025, are exempt from the new material assistance language.

- Two-year extension of clean fuel production tax credits, including for RNG, to December 31, 2029, provided feedstock is domestically sourced.

- Eliminates clean hydrogen incentives for projects that begin construction after December 31, 2027.

- Eliminates investment tax credit for Alternative Fuel Vehicle Refueling Property, which includes electric vehicle charging stations, for property placed in service after June 30, 2026.

The OBBB largely retains existing incentives for battery energy storage, with updates limited to revised FEOC rules. It also codifies pre-existing start of construction safe harbor interpretations, providing developers with greater certainty. While less sensational than other reports might suggest, the OBBB introduces meaningful, yet incremental, changes to the federal incentive landscape, consistent with the regulatory ebb and flow we have observed over our 25 years of investment management.

The OBBB supports North Sky’s infrastructure projects by enhancing incentives for clean fuels, maintaining a largely neutral stance on energy storage and instilling urgency for developers. This creates an investment opportunity to qualify both our existing and new solar projects for start of construction safe harbor treatment. Due to economic and policy considerations, we have not invested in wind for several years or pursued clean hydrogen and have no plans to start now.

We are fortunate to have ample liquidity in our Infrastructure Investment Fund (due to successful early exits) and SIF IV due to its recent final close. In Q2, amidst uncertainties surrounding the federal budgeting process, several reputable developers and operators—many long-term partners—approached us with liquidity needs for safe harbor projects and increased domestic content purchasing. Separately, the Liberal Party’s re-election in Canada in April 2025 bolstered the policy framework supporting clean fuel projects in our deal pipeline with Canadian offtake.

Special Reports. Our infra team authored two special reports in Q2. The First Report was issued in late April and provided a public policy update, underscoring that while the incoming Trump administration had made significant changes to the federal government, only a limited number of those changes directly impact sustainable infrastructure investors (some positively, some negatively but less than one might expect). The report also touched upon solar and battery tariffs and deregulation policy changes and described important positive developments at the state level in NY, IA, OH, MD and MT. The Second Report was issued on May 1 and delved into the need for significant additional infrastructure investments in America (a) to repair or replace outdated infrastructure that was originally constructed during the major public building programs of the mid-20th century, (b) to meet the rising demand for electricity due to the insatiable demand from AI and data centers and the ongoing Energy Transition (EVs, heat pumps, battery energy storage, solar power, etc.) and (c) to properly handle waste (municipal, industrial, agricultural, electronic and agricultural).

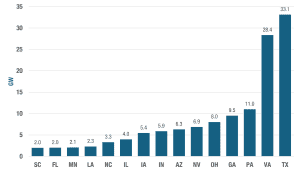

Data Center Conundrum. Plans to build new data centers are front of mind for developers, utilities, grid operators, legislators and regulators. As demand for power grows, local utilities struggle to accurately predict that growth and build sufficient generating capacity to power it. They also must contend with variability of demand from some data centers, which can have 25-30% swings in demand over just 3-5 minutes. When that variability comes from a hyperscale data center that can mean a 150-200 MW swing in load!

New Data Centers Announced in Top 15 States (130+ GWs)

Source: Wood Mackenzie

So how do we reliably and responsibly power, cool and integrate these data centers into the grid? Gas and coal power plants take multiple years to build but they can provide baseload power. While solar and wind power have shorter permitting, construction and regulatory hurdles, that power is obviously intermittent and requires energy storage to balance. Large scale nuclear plants have taken a decade or more to construct, primarily due to permitting and regulatory delays. The most recent nuclear plant to come online in the U.S. was in July 2023 in Georgia (1.12 GWs). It took 15 years to complete, more than double the initial timeline, and cost about $18 billion. The most recent new nuke plant prior to that was built in 2016 in Tennessee (1.15 GWs). Small module reactors (“SMRs”) are also being considered as part of the solution for powering new data centers, promising faster deployment, enhanced safety and a more flexible power solution compared to traditional reactors. Companies offering SMRs include NuScale, Oklo, TerraPower, BWXT, X-energy, Holtec, GE Vernova and Westinghouse. The free market may already be stepping up to help solve this problem. Emerald AI recently came out of stealth mode to announce that it can flexibly and intelligently adjust AI data center power demands to match available power from the local grid, primarily by choreographing workloads coming through Nvidia chips and prioritizing which tasks needed to happen immediately and which ones were not time sensitive and could be delayed.

We believe our infrastructure team can play a meaningful role here through our efforts in solar, energy storage and RNG and that our impact secondaries team can do the same through cooling, water use, energy efficiency, cybersecurity and dynamic load management companies.

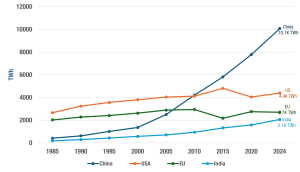

China Leads in Electricity Generation. China produced 10,000 terawatt hours of electricity in 2024, which was more than the U.S., EU and India combined. China is sprinting ahead of the rest of the world in terms of electricity generation to power its factories, its rising consumer class and, of course, AI. It uses an “all of the above” generation strategy, which includes coal, natural gas, nuclear, geothermal, wind, solar and hydro power.

Annual Electricity Generation by Country

Source: Visual Capitalist, our World in Data, North Sky Capital

China has nearly tripled its nuclear power capacity in the last 10 years such that it can produce 53 GW of power from 55 operating plants today. It has 23 more nuclear plants currently under construction and a stated goal of producing 200 GWs of electricity from nuclear power by 2035. Nuclear power will also help China pivot away from coal and its associated environmental concerns. China is currently building about two-thirds of the world’s wind and solar projects and has an installed base of about 880 GWs of solar power and 521 GWs of wind power. It also invested a massive $85 billion in grid transmission expansion and modernization. The West should invest in electricity generation and grid infrastructure if we want to win the AI race and have our world view be pervasive, rather than that of the Chinese Communist Party.

Paddle Energy. Paddle Energy, our solar development affiliate, advanced projects in Maine and Maryland and expanded into the Pennsylvania market during Q2. Pennsylvania’s Net Energy Metering regulation supports production revenue for solar projects under 3 MW, aligning with Paddle’s target project size. To support Paddle’s development efforts, North Sky’s Infrastructure Investment Fund increased its commitment to the Paddle joint venture by $2 million in Q2. Additionally, Paddle anticipates selling the first of nine Maine projects to a strategic acquirer by mid-July, a key milestone that will validate both Paddle’s strategy and the Maine market. The remaining projects are slated for sale upon development completion, scheduled between Q3 2025 and Q2 2026.

Buyer’s Market Continues. The buyer’s market continues for impact secondaries, and we are actively putting the remaining capital for Clean Growth VI (“CG VI”) to work now. We are finding high-quality impact assets at meaningful discounts to net asset value for fund portfolios and smaller, yet still attractive discounts and entry points for more concentrated transactions with 1-4 underlying companies. There are also positive signals for liquidity happening for our more mature funds, Clean Growth III-V.

To set the stage, we note that it has been a rocky road for many primary impact investors over the last five years—especially for investors in impact funds utilizing venture and growth equity strategies, which were adversely impacted by the rapid interest rate increases needed to cool the inflation caused by massive government spending that accelerated during and after the COVID pandemic. Those rate increases caused a devaluation of high growth assets, leaving many venture-backed companies unable to raise new capital unless they reduced their valuation below that of the prior financing round. Other companies were even less fortunate and were unable to raise necessary capital at any price, requiring a fire sale, bankruptcy or similar offramp. While the impact created by some of these firms has been outstanding, the investment returns and lack of exits have been disappointing in many cases.

Asset Class Trends (some of which play into our hands):

- Early-stage impact VC funds raised a tremendous amount of capital from 2018-2022, mostly for funds focused on climatech and energy transition. There were many emerging managers (i.e., less experienced teams) in this group as well. This vintage of funds invested during a peak in the valuation cycle. Now mid-cycle, many of these funds lack adequate capital to support their companies long enough to reach a successful exit, and the belt-tightening has started. Unsurprisingly, these funds typically have underperformed their investors’ expectations regarding IRR, MOIC and/or DPI. Many of these managers would like to raise a follow-on fund, which will be challenging given the underperformance and lack of liquidity. If they have institutional investors who decide not to re-up into the new fund, those institutional investors today often recategorize the old fund as “non-core” and begin to seek a buyer for it. This cycle has already begun, and we are seeing an uptick in this type of LP secondary deal flow.

- Growth Equity. This investment strategy has experienced some of the biggest growth within the impact community over the last few years and has been dominated by some of the big multi-strategy firms such as General Atlantic, TPG, Apollo and Apax. These growth equity funds are generally investing across multiple impact themes and are well positioned today if they have dry powder to take advantage of the plight of the early-stage venture funds of 2018-2022 (mentioned above). We are seeing strong deal flow in this “missing middle” category as well.

- Twenty years on, there is still a limited universe of impact buyout managers globally, with a handful of choices in the U.S. and more in Europe. The Wall Street firms offer some mid-market options, often exuding a bit of greenwashing. European managers skew more towards lower middle market and tend to be more authentically impactful, in our opinion. We see a smattering of buyout secondaries opportunities every quarter and would categorize this sector as trending slightly upward in terms of deal flow.

- Corporate Venture Capital Arms. We know several of these groups are being shut down now due to tighter capital availability and lack of exits. Our preferred way of transacting with them is to lift out the portfolio, and in certain cases the existing team, at a massive discount or effectively do the same thing through a structured transaction where we provide only partial liquidity to the corporation but have a 2-3x preferred return.

- In 12+ years, we have yet to see an infrastructure secondary opportunity that meets our high private equity IRR and MOIC thresholds, without taking undue risk. But we suspect the recent chaos created by the OBBB and related policy changes will provide new opportunities for us. As the need arises, we benefit from the insights of our Sustainable Infrastructure team as part of our secondary diligence process.

Exit Environment Commentary. While many of the headwinds that surfaced in Q1 and detailed in this commentary remain (e.g., policy changes, tariffs, trade negotiations and interest rates), we have seen a noticeable uptick in exit activity in recent weeks. This started with several high-profile IPOs, including some companies that have an impact angle, and has extended to traditional M&A transactions. Recent examples within our Clean Growth portfolio include Denso’s acquisition of Axia Vegetable Seeds (CG V) and MISUMI’s acquisition of Fictiv (CG VI). With the OBBB signed into law, we expect this will clear the way for more transactions in the back half of the year and anticipate all four of our secondary funds will make meaningful distributions to investors prior to yearend.

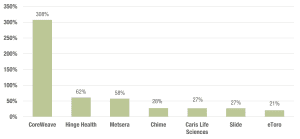

Strong Post-IPO Performance of Recently Listed Impact Companies

Source: Pitchbook. As of 6/30/2025

Clean Growth VI Update. We are very pleased with the early performance of the fund and believe that its diversification across impact themes and geography is proving valuable in this tumultuous period. While building and servicing renewable power generation assets is an important part of the impact ecosystem, we have long pursued companies that don’t rely heavily on favorable tax policy, including recycling, waste-to-value, water infrastructure services, education, healthy/better-for-you food/consumer products and healthcare service companies. Below are illustrative companies that CG VI now has exposure to through recent investments:

- Aloha = organic, plant-based protein bars

- Western Smokehouse = grass-fed protein snack manufacturer

- Amlon Group = waste management and recycles metals, oil and water

- Sentry Aerospares = recycles/reconditions spare parts for the aviation industry

- Kin Insurance = high catastrophe home insurer (climate adaptation)

- RapidSoS = public safety location services

Our proactive sourcing efforts are also uncovering opportunities in smart packaging, PFAS cleanup, connected homes, grid intelligence, cybersecurity, heating & cooling, remote asset monitoring, robotics & automation, weather intelligence, storm proofing physical infrastructure, value-based care, personalized medicine, non-toxic consumer products, behavioral & mental health, personalized learning and workforce training.

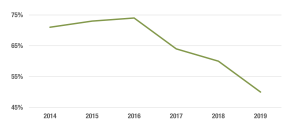

The Road Ahead. While there is some recalibration ongoing in the U.S. in a handful of sectors due to the OBBB, the opportunity set for impact secondary investors is vast and growing. First, the impact investment marketplace is global and we are seeing terrific opportunities across North America, Europe and in other developed markets right now. Second, the ongoing dearth of private equity exits means big investors are looking to the secondary market to free up cash. Average hold times have lengthened (worsened) such that, at the five-year mark, only 50% of 2019 vintage fund holdings had achieved full or partial exits on their holdings compared to more than 70% of 2014 vintage funds at their five-year mark. Looking at our deal sourcing pipeline, this lack of liquidity and the macro noise/uncertainty is creating a growing amount of deal flow from a broad base of impact investors.

Assets Partially or Fully Realized at Holding Period of 5 Years

Source: Bain & Company, “Global PrivateEquity Report 2025.”

Third, about $1 trillion was committed to impact funds over the last decade and many of those funds are in the sweet spot where they either have one or more investors who need liquidity or they have a general partner (a) looking to do a continuation vehicle with one or more of the premiere companies in the portfolio or (b) in need of additional capital in the form of a NAV loan or preferred equity infusion to support growth of their current portfolio.

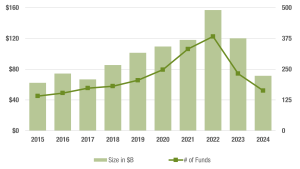

$1.0T Committed to 2,200 Impact Funds (2015-2024)

Source: PitchBook, “Q2 2025 Pitchbook Analyst Note: The State of Sustainable Investing in Private Markets.”

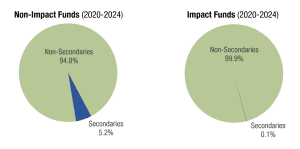

Fourth, impact investing has become very mainstream over the last decade but is still a nascent market compared to older alternative investment sectors like venture capital and buyouts. Although we created this niche impact secondaries market in 2013, we still have almost no competition and plenty of “white space.” When compared to all capital raised by impact funds over the last five years, impact secondaries funds were a tiny fraction of that—just 0.1%. In contrast, traditional secondaries funds from managers like Strategic Partners, Coller, Ardian and Lexington make up about 5.2% of the capital raised overall by non-impact funds. Thus, limited impact secondary competition and a chronically undercapitalized impact secondary market is expected to keep the pricing power in our hands for the foreseeable future.

Source: PitchBook, “Q2 2025 Pitchbook Analyst Note: The State of Sustainable Investing in Private Markets.”

Conclusion

The second quarter was a roller coaster but that wild ride is creating new opportunities. Now that the OBBB has been signed, some much needed certainty is here. We look forward to the remainder of 2025 and putting capital to work on behalf of our investors in SIF IV and CG VI.