Introduction

We are launching into summer with good news across multiple fronts.

North Sky News

Today, we are seeing important advancements in the following sectors:

• Clean Growth VII:

– The first investments are complete, creating immediate value appreciation

• Clean Growth VI:

– Final investments were approved in Q1

– The fund received distributions from Angel MedFlight, Amlon and Power Plus Communications in June

– We are tracking several active sale processes that, if completed as anticipated, should drive material distributions to LPs later this year

• Clean Growth V:

– EnergySolutions is expected to produce a significant gain to CG V when its announced acquisition closes

– Factorial Energy went public—see below

• As this commentary went to press, the IPO of Neutron Holdings (Lime electric scooters) was pending. The company (Ticker: LIME) has grown rapidly, with revenue rising from $522 million in 2023 to $887 million in 2025. It is held in both CG V and VI

• Our sustainable infrastructure team is finding attractive new investment opportunities in energy storage and EV charging

• Ava Salay and Charles Thorsen joined us as summer interns in our Wayzata, MN office

• We released our 2026 Impact Report—read it here

EV Battery Advancements

Battery advancements seem to be happening at a quickening pace, making EVs even more appealing compared to gas-powered cars. Notable cases this quarter:

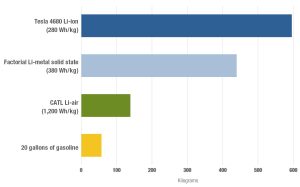

- Conventional lithium-ion batteries. Tesla achieved an engineering breakthrough to eliminate the toxic, energy intensive, wet slurry process used to make cathodes for lithium-ion batteries like its 4680 cells. The new dry process shrinks the manufacturing line, cuts cathode production costs in half (a significant overall cost reduction) and is already being used in cars rolling off the assembly line at Gigafactory Texas. Tesla’s 4680 cells have an energy density of about 280 Wh/kg. H/T The Electric Viking.

- Lithium-air batteries. CATL, the world’s largest battery manufacturer, announced an eventual pivot to lithium-air technology, with a theoretical energy density of 12,000 Wh/kg, which is virtually identical to the energy density of gasoline and jet fuel. These batteries use a lithium metal anode, a porous carbon cathode and pull oxygen directly from the atmosphere to use as a cathode reactant, effectively eliminating the need for heavy cathode compounds like nickel or cobalt oxides. This significantly reduces cell weight compared to conventional lithium-ion designs. CATL’s prototypes have already reached over 1,200 Wh/kg — four times the energy density of most batteries in commercial use today, and significantly higher than the 350-500 Wh/kg expected from solid-state batteries like those from Factorial Energy. If commercially scaled (perhaps by 2030), CATL’s technology would allow EVs to practicably travel 500 miles on a single charge and would significantly enhance the use case for electric aircraft beyond the short hops currently contemplated by companies like Joby Aviation (150 mile range) and Archer Aviation (60 mile range).

The transition for gas-powered cars to EVs has been progressing gradually over the last 15 years but, with sufficient battery advancements, that transition could accelerate dramatically. One of the main resistance points has centered around the fact that you need a very large (heavy!) battery for an EV to travel similar distances to regular cars. The chart below shows the impact of moving from the current state-of-the-art for batteries (Tesla) to solid state batteries with higher energy density to CATL’s Li-air batteries with tremendous energy density. Our illustrative chart is based on a 20-gallon gas tank in a car that gets 25 MPG (i.e., 500 miles per tank of gas and that fuel weighs 57 kg). To get the same range in a Tesla would require nearly a 600 kg battery, but CATL’s new battery would be far lighter, just 139 kg. Note, we are not factoring the weight difference between an internal combustion engine/multi-gear transmission and an electric motor/single-gear transmission, which would slightly benefit the EV in this analysis.

Weight of Gasoline or Battery Needed for a 500-mile Drive

Market Update

A Welcome Shift in Market Dynamics

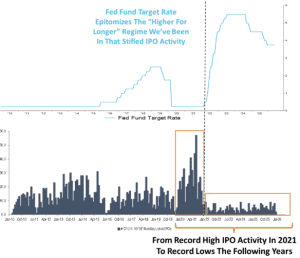

IPO Activity. We have good news to report regarding Q2 IPO activity. Several bellwether climatech companies went public in Q2, including some of our own portfolio companies. We believe this signals a meaningful shift after years of suppressed IPO activity:

- Factorial Energy (FAC), solid state batteries for drones and cars (CG V)

- ERock (EROC), microgrids for data centers

- Fervo Energy (FRVO), Geothermal energy

- X-energy (XE), small modular reactors and nuclear fuel pellets

- Deep Fission (FISN), small underground nuclear reactors

- SpaceX (SPCX), spaceflight, telecom, ISP and AI (originally was in PEP III (2006 vintage))

This is welcome data since there has been a dearth of IPO activity since the Fed cranked up interest rates in 2022. See illustrative charts below from Piper Sandler.

IPO Activity Came to a Halt Following the Fed’s Most Recent Hiking Cycle

A Potential Inflection Point. High-growth companies are attractive IPO candidates, but they are highly sensitive to interest rate movements—a dynamic longtime readers will recognize from our commentary over the past several years. Based on conversations with investment bankers, fund managers and portfolio company CEOs, the recent SpaceX IPO may be a harbinger of improved liquidity conditions. Other factors support this view: strong investor appetite for the expected IPOs of Anthropic, Databricks and other AI-adjacent companies, the winding down of the Iran war, oil prices falling below $70 a barrel, strong jobs numbers, relatively tame inflation and new Fed Chair Kevin Warsh signaling the markets should be allowed to be more independent rather than guided by the Fed.

Emerging Risks Deserve Attention. That said, we are operating in a complex, fast-moving, and volatile environment. New risks have emerged that buyers must weigh carefully:

- Geopolitical tensions and energy/supply shocks

- The potential of an AI valuation bubble, market concentration risk and specifically AI’s effect on the long-term value of certain sectors such as software

- Inflation persistence and monetary policy risks

- Economic slowdown or recession risks

- Stock market volatility and market correction risks

- Political instability in Western countries due to historic levels of immigration, and the downstream effects on wage levels, housing, healthcare, education, crime and social services

- Policy and regulatory uncertainty surrounding tech, trade and labor

We expect these uncertainties to continue weighing on deal activity, extending hold periods across the market.

A Cautiously Optimistic Consensus. The consensus among alternative asset managers is cautiously optimistic: 61% of PE firms surveyed by Piper Sandler anticipate improved exit conditions in the next six months, and half have identified portfolio company exits as a key priority. However, this optimism must be tempered by the reality that exits are likely to remain concentrated among large, high-quality assets, while smaller non-portfolio drivers will need to reduce valuation expectations to achieve liquidity.

North Sky’s Role in this Environment. Secondary managers like North Sky are well-positioned to play a critical role in this landscape. We provide liquidity precisely when it is needed most—during windows when macro headwinds delay exits but underlying portfolio value remains intact, and when strategic buyers are on the sidelines. Our ability to see through the headline noise—macro, geopolitical or otherwise—allows us to deploy capital at attractive valuations when others pull back.

For our portfolio, our role is twofold:

- Support long-term value creation. We partner with managers to support sustainable, durable value creation in their portfolio companies and help them resist the temptation to force exits into unfavorable windows.

- Preserve optionality. We ensure our underlying managers and their portfolio companies are positioned appropriately for when windows of favorable liquidity open—whether through strategic M&A, IPO or secondary sale—by maintaining disciplined operational focus and optionality around exit timing.

The companies generating meaningful returns in this environment are those led by managers with both patience and strategic flexibility. We are committed to supporting that balance. As the exit backlog continues to build and policy uncertainty persists, a trusted secondary partner has never been more valuable—one who provides flexible, collaborative secondary solutions and remains patient and supportive after the deal closes.

Secondary Market Volume Surges 42% to $220 Billion

The global private equity secondary market hit $220 billion in transaction volume in 2025—up 42% from 2024—and is projected to reach $250 billion in 2026, according to William Blair’s annual secondary market survey.

Notably, 91% of respondents said geopolitical and macroeconomic turbulence (tariffs, Ukraine, Middle East) has not changed their activity, underscoring the market’s resilience. Europe is emerging as a major growth area, with $60 billion in 2025 volume and half of survey respondents planning to expand their European presence in the next year.

Looking further out, William Blair projects the market reaching $400 billion by 2030, driven by the maturation of continuation funds, growing use of secondaries as an ongoing portfolio management tool rather than a one-time liquidity event and the entry of retail capital into private markets generating sustained LP liquidity demand.

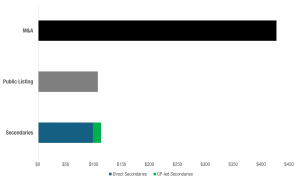

Separately, Pitchbook reported that on an annualized basis, venture capital exits to secondary funds ($112.6B) exceeded IPO exits ($106.6B) for the first time ever. While some of that secondary activity was due to heightened interest in SpaceX, Anthropic and OpenAI, our read of the data is that secondary exits are now ensconced as a significant exit pathway for the VC community. The data was measured across the four quarters ending on March 31, 2026.

US VC Exit Value by Type Q2 2025 to Q1 2026

Source: Pitchbook

Artemis II and Aerospace Investment Opportunities

The Artemis II lunar mission is also worth mentioning. It launched on April 1 from Kennedy Space Center and was the first crewed flight beyond low Earth orbit since Apollo 17 in 1972. It captivated the world during its 10-day journey to the moon and reinvigorated the NASA space program, further spurring interest in space exploration and aerospace innovation. Once again, we are dreaming big dreams such as establishing a moonbase, data centers in space, missions to Mars and mass drivers (basically lunar railguns used to launch payloads without rockets). Ten years ago, that seemed pure fantasy, but the success of the Artemis II mission showed us we are only limited by our imagination and willpower. The explorer in all of us—the desire to stretch the boundaries of human existence, capability and understanding—has been rejuvenated. North Sky has invested in adjacent areas like rocket recovery/reuse, last mile delivery/logistics, battery tech for aerospace, aircraft parts and wind turbine maintenance by drone (MMIST, Zipline, Amprius, Sentry Aerospares and Gadfin, respectively).

Kennedy Space Center, March 2026

Infrastructure Supercycle

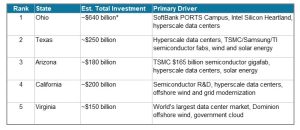

The United States is undergoing the largest coordinated infrastructure investment cycle in its history, driven by the convergence of artificial intelligence compute demand, domestic semiconductor reshoring under the CHIPS and Science Act, the clean energy transition accelerated by the Inflation Reduction Act, and federal Bipartisan Infrastructure Law allocations. Across all 50 states and four investment categories—Data Centers, Energy Infrastructure, Semiconductors and Energy Transition—total announced and committed investment from 2020 through 2035 is estimated at approximately $2.3 trillion. Five states account for most of this capital: Ohio, Texas, Arizona, Virginia and California. Together, they represent an estimated $1.42 trillion of the national total, driven by landmark semiconductor mega campuses, the world’s largest AI data center markets and transformational clean energy commitments.

The investment landscape is uneven. Northern Virginia alone hosts more than 35% of global data center capacity, making it the single most important digital infrastructure market in the world. Arizona has attracted the largest foreign direct investment in a greenfield project in U.S. history with TSMC’s $165 billion semiconductor campus in Phoenix. Ohio is the site of what may become the largest single construction project in American history, anchored by SoftBank’s PORTS Technology Campus in Piketon. Texas leads the nation in both renewable energy capacity and hyperscale data center square footage, with more than $250 billion in combined commitments. California, while constrained by power availability and permitting, retains its position as the global epicenter of semiconductor design, AI research and clean energy policy leadership.

Federal programs have been decisive catalysts. The CHIPS and Science Act has directed more than $52 billion in direct funding and loan guarantees to domestic semiconductor manufacturing, with the largest single awards going to TSMC Arizona ($6.6 Billion), Micron New York and Idaho ($6.1 billion), Samsung Texas ($6.4 billion) and Intel across Ohio, Arizona, New Mexico and Oregon ($7.9 billion). The Inflation Reduction Act has deployed trillions in tax credits that have attracted solar, wind, battery storage, EV manufacturing and clean hydrogen investment in virtually every state. The Bipartisan Infrastructure Law has delivered critical grid modernization, broadband, water and transportation funding, particularly to rural and historically underserved states. This is a rich terrain for North Sky’s infrastructure team.

Top 5 States by Total Announced Investment

*Includes SoftBank CEO Masayoshi Son’s stated $500 billion full-campus ambition for the PORTS Technology Campus. Phase 1 confirmed spend is $30 to $40 billion. All figures are announced commitments, not fully deployed capital.

Source: North Sky Capital research

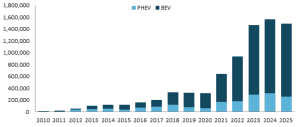

Electric Vehicles

U.S. EV sales, including battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs), rose roughly 13x from approximately 115,000 units in 2015 to 1.6 million in 2024—a compound annual growth rate near 30%—before easing to approximately 1.5 million in 2025, as the phase-out of the $7,500 federal tax credit in late September pulled demand forward into the third quarter and suppressed fourth-quarter volumes. The EV market continues to mature: nearly 90 EV models are now available, up from fewer than 30 in 2020; Ford, GM, Toyota and Hyundai have each committed to electrification through 2030; the North American Charging Standard—compatible with different auto manufacturers and both AC and DC charging—has become the standard industry connector; and late last year EV market share topped 10% of new vehicle sales for the first time.

Annual EV Sales in the US

Source: Light Duty Electric Drive Vehicles Monthly Sales Updates | Argonne National Laboratory

Demand for charging infrastructure globally grows with each new EV sold. EV adoption has somewhat outpaced the build-out of charging stations in the U.S. By comparison, China and Europe have 2-3 times the charger coverage. We expect 2026 will mark a shift of new-build emphasis from single family garage chargers to apartment/multifamily and workplace charging infrastructure. We also expect a shift from rural DC fast charging corridors to more capital efficient urban level 2 charging. The charging infrastructure market is maturing from “build it and they will come” to more targeted build-outs of locations with strong unit economics and utilization data and in cooperation with landlords and corporate property owners such as big box retailers.

Charging equipment costs continue to decline, though somewhat offset by increasing electrical labor and make-ready costs. Site selection evaluates the age of sites and seeks to build under Utility Make Ready programs, which reimburse the electrical scope (panel upgrades, conduit, wiring and metering) required to bring a site to a charger-ready state. From the utility’s perspective, chargers add load to the distribution system, improve grid utilization and help satisfy state clean-energy mandates.

Our infrastructure team has been evaluating the EV charging sector since 2021, and SIF IV is finalizing an equity investment in an existing portfolio of charging stations with attractive expansion opportunities in partnership with large corporations.

Solar

The latest U.S. Solar Market Insight report from the Solar Energy Industry Association (SEIA) and Wood Mackenzie showed the country added 7.8 GW of solar in the first quarter of 2026 and crossed 6 million cumulative installations. Solar and storage together accounted for roughly 91% of all new generating capacity added to the grid in the quarter, and contracts for utility-scale solar rose about 15% year over year as technology companies locked up power for their AI computing needs.

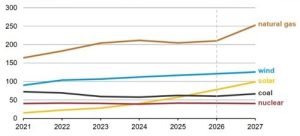

In its May 2026 Short-Term Energy Outlook, the US DOE’s Energy Information Administration projected that annual utility-scale solar generation in ERCOT (Texas) will surpass coal for the first time in 2026—78 billion kWh from solar versus 60 billion kWh from coal; and widening to 99 kWh versus 66 billion kWh in 2027. With no new coal plants planned in ERCOT, and Texas expected to account for roughly 40% of all new U.S. solar capacity additions this year, the structural shift is clear. SIF IV owns nearly 1 GW of ERCOT storage development assets positioned to manage the mismatch between mid-day solar generation and peak demand hours, as well as supporting grid reliability during rapid net-load changes. Further, the growth in ERCOT’s large load queue, even beyond what was highlighted in our Q1 market commentary, is creating a steeper duck curve—the intraday increase in power demand unmet by solar as the sun sets—heading into 2030. This phenomenon is especially pronounced in the West and the Panhandle with its concentration of data centers, and it justifies charging batteries with midday sun then discharging them later in the day.

Annual Electric Power Generation in ERCOT

billion kilowatt hours

Source: U.S. Energy Information Administration

State Regulatory Matters

New York and Maryland both enacted meaningful pro-solar legislation with direct benefits to IIF and SIF IV portfolio companies.

New York’s FY2027 budget commits $200 million to the NY-Sun program, supporting roughly 1 GW of new rooftop and community solar while leveraging an estimated $1.5 billion in private capital. Complementary grid modernization measures increase solar hosting capacity by up to 3.3 GW upstate and storage integration in Con Edison territory by 274%, with projected ratepayer savings of $1 billion annually. The NY-ISO’s June Power Trends report underscored urgency, forecasting capacity shortfalls under extreme weather scenarios.

Maryland’s Utility RELIEF ACT doubles distributed solar capacity to 6 GW under NEM 1.0 and 2.0. Critically, existing projects are grandfathered under NEM 1.0 rates until decommissioning—an accretive outcome for current IIF and SIF IV holdings.

Conclusion

As we conclude this quarter’s market commentary, we wanted to thank FIFA and all the soccer fans who have poured into North America for the World Cup. As such, we are getting to celebrate America’s 250th birthday together with friends from around the world. It has been fun to read visitors’ social media posts as they discover our national parks and scenic byways and partake in American culture, often far from the usual tourist destinations like NYC and LA. Who knew Buc-ee’s, free refills on soda and American hospitality would be such a sensation?

America was founded 250 years ago with the signing of the Declaration of Independence. The core principles of which are:

- All men are created equal

- They are endowed by their Creator with certain unalienable Rights, among which are life, liberty and the pursuit of happiness

- Government is meant to protect these rights and derives its power from the consent of the governed

- Whenever a government becomes destructive of these ends, it is the right of the people to alter or abolish it and to institute a new government

Those core principles, drawn from Aristotle, Cicero, Locke, Rousseau, Hobbes and other contributors to the Enlightenment, ring even more true today, at home and around the world.

As we wrap up the first half of 2026 and launch into the second half, we are enthused by the flurry of climatech IPOs which seem to signal a liquidity thaw and the generally favorable market, economic and regulatory landscape. The energy and AI infrastructure supercycle is real and accelerating. Battery technology and automation are advancing rapidly. The companies in our portfolio are positioned at the intersection of these tailwinds with real momentum behind them.

The world is complex and the investment environment is ever-changing. But complexity is where patient, disciplined investors with deep domain expertise earn their stripes. We built North Sky to thrive in these conditions. Our ability to source investment opportunities, see through headline noise, deploy capital at attractive valuations and support our managers, projects and portfolio companies through these volatile conditions is a competitive advantage.

Happy 250th, America, and thank you all for joining us on this journey.