Introduction

Wow, what a quarter! Q4 was jam-packed with big news and events. We attended SOCAP 24 in the Bay Area and re-connected with many of our investors, advisors and friends. We visited investors in London, NYC, Chicago, St. Louis and Washington, DC. Our sustainable infrastructure team signed two letters of intent for new investments and completed a partial sale of our Orenda battery storage projects. Our impact secondaries team approved three new investments (two of which closed in Q4), and we sold our long-standing interest in Ecore International, the premier tire recycling company in the USA, for a significant gain. Kudos to Michael Derosa and Art Dodge at Ecore / CommonWealth Equity Partners.

The price of one Bitcoin surpassed $100,000 for the first time ever, grabbing the attention of investors, central bankers, policymakers and Wall Street. Cathie Wood, CEO of Ark Invest, maintains her $1mm price target for Bitcoin by 2030.

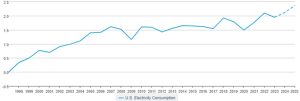

There were massive leaps forward in quantum computing and Artificial Intelligence (AI) during the quarter. AI and electric vehicles (EV) require a lot of electricity, so we are expecting to see the demand curve for electricity bend upward again after several years of relatively flat demand.

US Electricity Consumption

Indexed to 1997 as value

billion kilowatthours per day

Source: US Energy Information Administration

That increased demand creates investment opportunity for both of our investment teams. For example, we are seeing more EV charging, energy storage and data center opportunities, with the latter needing to be cooled and powered using sustainable methods. McKinsey & Co. believes energy demand from data centers will grow from 4% of total US electricity consumption today to 11-12% by 2030. All of this is prompting hyperscalers like Google, Microsoft, Meta and Amazon to take an “all of the above” approach to powering their datacenters, including renewed interest in nuclear power ranging from bringing Pennsylvania’s Three Mile Island Unit 1 nuclear reactor back online to more advanced approaches like small module reactors from Oklo Inc.

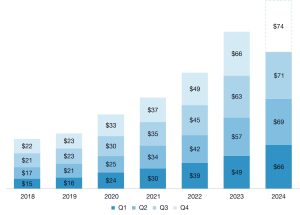

In late November, public reporting confirmed what our infrastructure team already knew—that clean energy and transportation investment in the USA was reaching all-time highs with a record-setting $71B invested in Q3. Extrapolating year-over-year gains from Q3, one would expect $74B of investment in Q4.

Clean Investment by Quarter

Billion 2023 USD

Source: Rhodium Group, MIT Center for Energy and Environmental Policy Research and North Sky Capital

Solar power continued to make impressive headlines, including the first commercial sales of perovskite solar panels, which are purported to be (1) 20% more powerful than conventional silicon modules, (2) 24.5% efficient at converting photons to electrons and (3) durable (high degradation was perovskite’s historical weakness). We also applaud our friend Dan Shugar and his team at Nextracker (ticker: NX) for launching a 100% made-in-America solar tracker system, enabling solar developers to receive an additional investment tax credit for using such systems in US projects.

Past portfolio companies, SpaceX and Tesla also had big events. SpaceX successfully landed the Super Heavy rocket booster for its 400-foot-tall Starship vehicle—or rather caught it with mechanized chopsticks—in October. The technical prowess to do this marks a seminal point in human history and is worth re-watching here. Tesla held its CyberTaxi event where it unveiled autonomous taxis with a massive trunk, robot bartenders and a new RoboVan prototype.

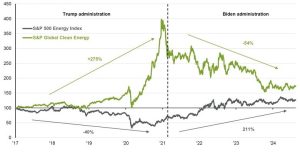

The USA held its elections in November, and we now have the answer to who will be the next President. This feels like a “back to the future” moment but we know that change provides opportunity. Also, it is worth noting that If you had guessed in 2016 that a Trump presidency would be bad for clean energy investors and good for traditional energy investors, you would have been wrong. Had you guessed the opposite in 2020 about the Biden presidency, you would have also been wrong. Please see the interesting chart below from FactSet / JP Morgan and also our public policy update regarding what to expect from Trump’s second term.

Traditional and Renewable Energy Performance

Indexed to 100 on 1/20/2017

Source: Factset. JP Morgan Asset Management. Data are as of September 30, 2024

There were also some negative headlines in the broader impact segment: Northvolt and Lilium filed for bankruptcy. Northvolt is a Swedish maker of battery cells for electric vehicles that hopes to slim down through a restructuring of its roughly $6B in debt. Lilium is a German manufacturer of electric, short-haul jets that still plans to hold its first crewed flight in 2025. Neither company was a portfolio holding of ours, but we are intimately familiar with them given our long-standing investment activity in the energy storage and next-gen mobility sectors. We hope both companies continue operations and emerge stronger on the other side of the bankruptcy process.

Personnel. We added Jessica Ingram as a Senior Advisor in Q4. Jess has over 15 years of solar development expertise and prior to joining our affiliate Paddle Energy as Chief Operating Officer, she was the Senior Director of Development at Cypress Creek Renewables.

Secondaries Whitepaper. We authored a secondaries whitepaper, intended as a primer on private equity secondaries investing for those investors who are still unfamiliar with this method of investing. Next quarter, we will publish a follow-up whitepaper on the benefits of investing in specialty secondaries funds, such as our series of impact secondaries funds.

New Markets Tax Credits. During Q4, we were awarded $40mm of New Markets Tax Credits for the firm’s Low Income Communities initiative, which allocates new market tax credits to underserved, mostly rural, communities through our National Impact Fund subsidiary. To date, we have allocated nearly $100mm to a variety of projects, including capital for the purchase of new manufacturing equipment to enable job creation at the American Spiralweld plant (Paris, TX), the replacement of the wastewater treatment plant for the benefit of the Navajo Nation (Kayenta, AZ) and, most recently, construction of the 100,000 square foot addition to the Harry Chapin Food Bank (Fort Myers, FL).

Market Update

The fourth quarter, and indeed all of 2024, yielded strong results for our infrastructure team and our underlying portfolio of investments. Throughout the year, we steadily put capital to work in energy storage, renewable natural gas, community solar and other related areas. We also sought exits for our more mature assets. Our market analysis of key trends in clean power, environmental infrastructure and grid optimization were also accurate, predicting strong growth in the areas of energy storage and clean power for data centers for example. Looking ahead to 2025, we are excited about the potential returns that we can generate by continuing to deploy capital in our sectors of focus and specifically the prospects for Sustainable Infrastructure Fund IV.

Energy Storage. Our infrastructure funds increased their exposure to lithium-ion battery storage more than they did to any other renewable sector in 2024. Our efforts in this sector were recently validated by a December liquidity event for some of our most mature storage projects in New York. Working with our development partner, we are rapidly and efficiently building more storage sites there (up to 40 sites in total). Further, we are in the final phase of adding another storage developer relationship in a new region and expect to announce that in our next market commentary.

Data centers are the foundation of our digital world, and the size of that foundation is growing by leaps and bounds. The growth in data center computing demand is largely driven by the growth in AI and a shift by some cryptocurrency miners to use data centers. Years ago, miners would typically use their own hardware and cheap, stranded sources of energy such as methane from oil & gas exploration that otherwise would have been flared on site. As costs and environmental concerns surrounding crypto mining mount, miners are increasingly utilizing data centers for the necessary computing power. Some of those data centers are specifically built for crypto mining, while others host users of all types. Those data centers can be cost-effective, highly efficient and powered by clean power sources. But to be optimized for renewable power, they need massive battery systems to store the electrons coming from intermittent sources like wind or solar so they can subsequently evenly dispatch that power 24/7. As regional electric grids like Texas shift to more renewable resources, battery storage systems are needed more and more.

Power Demand Growth. As shown in the Electricity Consumption chart above, the USA is experiencing meaningful macro-growth in electricity demand for the first time in many years. During the 2010’s the energy transition was largely a rotation away from fossil fuels and into renewables. This rotation is still ongoing but is now happening within a growing total market, driven largely by computing and EV energy demand. Q4 saw the continuing maturity of data center infrastructure as a private investment opportunity, with large investors such as Global Infrastructure Partners, GIC (Singapore’s sovereign wealth fund) and Canadian Pension Plan Investment Board announcing multi-billion dollar data center transactions.

Various studies predict AI power usage will add between 1.5-4.0% load demand to the grid by 2030. That equates to about 15-40 GWs of additional needed capacity. Importantly, new data center demand is not evenly distributed across the USA. Recently, we have seen actionable data center opportunities in Texas and Illinois. There is also a lot of new data center construction concentrated in states like Virgina, California, New York and Arizona. North Sky maintains developer relationships in all these regions, and we are actively seeking opportunities to create renewable power generation infrastructure alongside this load growth in 2025.

RNG For Gas Utilities. Renewable natural gas can play an important role in decarbonizing energy production from North American utilities. RNG typically is derived from wastewater treatment plants, waste processing facilities or landfills. During 2024, we made significant progress at all our RNG project sites. This included our East Coast waste-to-RNG facilities that create RNG from food waste and other organic material and then sell that gas to Canadian utilities under long-term offtake agreements. On the West Coast, we benefited from the recent approval of an offtake agreement by the California Public Utilities Commission under Senate Bill 1440 (RNG biomethane procurement targets). This was the first such approval under that regulation and relates to industrial and pre-consumer food waste that is converted into RNG at our site in San Bernardino. The approval was an important regulatory milestone and affirms our current and planned RNG development efforts in California.

State Policy Support. State-level Renewable Portfolio Standards continue to supplement federal policy in enhancing the returns available to sustainable infrastructure investors. In December, the New York State Energy Research and Development Authority (NYSERDA) announced awards for offtake contracts for 23 renewables projects totaling 2.3 GWs of potential new capacity. North Sky solar counterparty Cordelio Power (owned by CPPIB) was a beneficiary of nine of the awards. All 23 awards were for land-based projects, consistent with North Sky’s view that offshore wind projects continue to face ongoing policy and economic hurdles—not to mention engineering, construction and operational challenges.

Exit Environment. We believe several key dynamics that resulted in below-average liquidity for private market investors over the last two years have recently improved and should support a rebound in M&A and IPO activity in 2025. In particular, inflation has trended lower, the Federal Reserve began a rate-cutting cycle, borrowing costs have come down and the incoming Trump administration and Republican-controlled Congress is being broadly viewed as pro-business with dual goals of increasing economic activity and reducing wasteful spending of taxpayer dollars.

From our vantage point, good companies are being sold quickly and at premiums as corporate and financial buyers look to get ahead of what may be a competitive 2025 for buyers. Conversations with several investment banks indicate they are entering 2025 with a full pipeline of M&A and IPO candidates with little room for new mandates.

Annual Meeting Season Takeaways. The majority of our underlying fund managers hold annual meetings during late fall. There were two notable takeaways from what we heard this year. First, the 2021-2022 vintage year is ugly. We consistently saw charts highlighting how frequently and consistently private financings were overpriced during this period. This is not new news. It does, however, feel as if managers are starting to lay the groundwork for why returns for these vintage years will be underwhelming and take longer to monetize. Second, a majority of the VC backed companies that were not yet profitable used the last 12-18 months to raise fresh capital and extend their cash runway. While many VC funds used this as an opportunity to reset the equity valuation, others opted for a “kick the can down the road” approach where structures like convertible notes, ratchets and participating preferred provisions were used to minimize or avoid a valuation write down for existing investors. This tactic was used in ServiceTitan’s final private financing, which was widely reported before the company’s IPO in Q4 We were not investors in ServiceTitan, just to be clear.

Buyside Considerations. Headline discounts for secondary transactions trended downward (smaller) throughout 2024 as macro and company conditions improved and new secondary investors, particularly evergreen strategies, entered the market. This was particularly the case for middle market buyout funds and a handful of high-flying tech companies that secondary investors were chasing (e.g., OpenAI, Stripe, Databricks, SpaceX, Redwood Materials and Anduril). This, however, has not been the case in our niche of impact secondaries. We continue to find attractive opportunities that span climate and health themes at material discounts. Uncertainty around the positive and negative effects the Trump administration may have on impact companies is a net positive for experienced impact investors like North Sky that have (1) invested through several impact waves with Republican- and Democrat-led governments and (2) the ability to conduct bottoms-up analyses on generalist impact portfolios. Consistent with prior quarters, our climate focus is on opportunities where underlying companies are cost-competitive with traditional alternatives and not reliant on government financial support or intervention. The most interesting opportunities are surfacing in recycling/re-use, grid electrification and infrastructure service companies today.

Commentary on GP- led Secondaries. Pitchbook’s latest GP-led Secondaries Report affirms the growing importance of continuation vehicles in the private equity exit landscape. Over the past five years, the total exit value from GP-led deals has more than doubled, while the number of exits has increased more than 5x. As a percentage of global exits, GP-led secondaries now account for 7.2% of total value (up from 2.7%) and 3.8% of total number of deals (up from 0.6%) over that same five-year period. Early returns from these GP-led secondaries look very attractive compared to other private equity options (primary funds, co-investments, etc.), thus propelling strong re-up rates for secondary fundraises.

More growth in GP-led secondaries is expected, potentially reaching $70 billion of total deal volume by 2028 (Pitchbook). This is in line with our expectations. We believe the trend towards larger transaction sizes will continue. This largely stems from private equity managers seeking to extend their ownership period of their best (and often largest) assets. This is typically done via a single asset continuation vehicle, followed by selling the rest of their portfolio investments in smaller clean-up transactions. During portfolio clean-up, those managers tend to be less price sensitive. North Sky is seeing opportunities in both the single asset deals and the clean-up transactions. But the latter are particularly appealing to us right now considering recent upward price movement (smaller discounts) for many single asset vehicles.

Conclusion

We ended the year strong and are incredibly optimistic about what 2025 holds in store for our sectors of investment focus. We wish all of you a happy, healthy and prosperous new year!