Introduction

The world seems awash in chaos and controversy. It has been a tough couple of years due to covid before and now inflation, supply chain problems, resource shortages and of course the Russia/Ukraine conflict. Inflation is an alarming problem, and we need more than political talking points to get it under control. Economist and author John Mauldin recently provided the following self-explanatory inflation chart in his Thoughts from the Frontline commentary.

Inflation has accelerated and is causing great harm to consumers and rattling investors. Poor and middle-income households suffer immensely when the cost of their food, fuel, clothing, housing, healthcare and other necessities increase by 10-40% seemingly overnight.

Inflation and recent stock market volatility are causing investors to re-evaluate their existing holdings and upcoming investments. As they do so, we encourage them to look at our investment strategies, especially our sustainable infrastructure strategy, which has inflation adjustment provisions written into the offtaker agreements for virtually all of our investment projects. Similarly, our impact secondaries strategy benefits from price instability and market volatility, which spurs some panic selling by others and also delays expected exits for companies resulting in opportunities for us to provide extension capital in the form of preferred equity and continuation vehicle investments. For investors seeking stability in these uncertain times, private market investments such as these have the potential to provide attractive returns and diversification away from a volatile stock market.

Looking past the headlines, one sees that we are in the midst of a transition to a renewable energy future, and that is a good thing if done intelligently. It can also go very poorly if not executed well. The Chinese Communist Party is outmaneuvering the rest of the world and only a few people in Washington, D.C., London and Brussels know this and are doing anything about it. The future is solar panels, EVs, batteries and the raw materials and factories needed to build them. The CCP has known this since 2008 and has taken methodical steps to build the factories, “acquire” the necessary intellectual property and secure the rights to massive quantities of the necessary raw materials (e.g., nickel, copper, cobalt, neodymium and lithium) to dominate this transition. America and the rest of the free world better get moving. We can build those factories, create high quality jobs and procure many of those resources ourselves in an environmentally responsible way. Let’s work together to make that happen.

Here at North Sky, we are doing our part. Our impact strategies are helping with the transition to a cleaner, more sustainable energy future. We are also creating jobs and generating attractive returns for our investors. If you haven’t already, we hope you join us on the next leg of this transition.

Market Update

Sustainable Infrastructure

As noted above, our sustainable infrastructure strategy is directly participating in the transition to a more sustainable energy future. The projects we develop and finance span important sectors like environmental infrastructure (renewable natural gas, water and waste to value), EV charging, community solar and energy storage. The transition to a renewable energy future is accelerating thanks to economies of scale, public awareness of its appeal and geopolitical events like the current oil and natural gas price shocks due in part to Russia’s invasion of Ukraine.

As an aside, we seem to be receiving a record number of inbound inquiries about our funds right now. Inbound inquiries tend to ebb and flow over time but we have noticed a strong correlation with oil price shocks over the last 17+ years. At $90 per barrel of oil, the phone starts to ring steadily. At $100 per barrel, it rings off the hook.

Spotlight on Energy Storage. We expect to close soon on an investment in a development pipeline of utility-scale battery projects totaling 200 megawatt-hours of capacity in a northeastern urban market. Battery projects earn revenue based on the value of providing on-peak electrons to the power grid. In many markets this value is expressed in the form of “capacity” prices, which are the payments made by the power grid to the battery for having dispatchable electricity generating capacity during hours of high demand. Recent capacity price volatility in certain markets created an opportunity for North Sky to acquire assets at a reasonable price.

Overall the energy storage market is experiencing supply chain constraints due to the impacts of covid and the Russia/Ukraine conflict. These constraints have caused lithium-ion battery manufacturers to raise prices in excess of 20%. We believe the industry will overcome these growing pains in due time, but the current difficulties suggest the need for additional near-term policy support. Further, lithium-ion battery production will increase, relieving some of this price pressure. The current environment also creates an opportunity for non-lithium technologies, especially in non-urban, non-commercial applications where energy density/ small footprint is less of a priority. Flow batteries with longer durations are positioned to compete with lithium-ion in these markets.

Spotlight on Organic Food Waste. Between 63 and 103 million tons of wasted food is generated annually in the U.S. from residences, restaurants, food manufacturers and large institutions such as hospitals, universities and government facilities.1 Over half of wasted food is presently sent to landfill, where it generates significant methane emissions.

In recent years, growing awareness and concern about landfill capacity and methane production have led an increasing number of U.S. states to tighten regulations concerning what can be landfilled. For example, California Senate Bill 1383, which was signed into law, stipulates that 75% of organic waste must be diverted to alternate uses by 2025.2 New York, Massachusetts, Connecticut, Rhode Island and Vermont have similar regulations in place, as do several large municipalities, such as Portland, Oregon and Austin, Texas.3 As states and municipalities increasingly mandate that organic waste be diverted from landfills to beneficial uses, new infrastructure is being created by North Sky and others to address these requirements.

There is a significant opportunity for us to deploy capital to address this need. For example, we can develop and construct organic waste handling, anaerobic digestion and methane upgrading facilities to properly deal with organic waste. Waste-to-energy and waste-to-value infrastructure typically takes organic waste and converts it into methane, fertilizer, animal feed and/or other beneficial uses.

Specific example: We are in formal negotiations to add another RNG project to our portfolio that will produce renewable natural gas (“RNG”) from local organic waste such as source-separated organics (“SSO”), and food residuals from municipal solid waste. Waste haulers pay tipping fees to the project to offload this waste. This project will retrofit an existing facility, which is favorably situated next to a large landfill, and will be able to process 104,000 tons of organic waste per annum. This will prevent roughly 6,760 metric tons of methane emissions each year, equivalent to removing 37,000 cars from the road, or planting 2.8 million trees.4 The facility will produce 337,000 mmbtu of RNG per annum and inject that gas into the local pipeline, displacing an equivalent amount of fossil fuel derived natural gas from the pipeline system. The project gas is expected to have a carbon intensity of between -40 and -80 grams of CO2 per Megajoule, which measures how much CO2 it displaces when compared with fossil fuels. The project has a power purchase agreement with a strong counterparty.

IIF Update. At yearend, our Opportunity Zone focused infrastructure fund closed on additional capital and the fund now totals $120 million in commitments. IIF has now invested in two projects (Golden Bear and North Farm) and has three additional investments in advanced diligence. IIF is closed to new investors.

We are Hiring. Our infrastructure team is seeking an experienced Associate level candidate. Qualified candidates must have two to three years of relevant work experience in one of the following areas: (a) investment banking or equity research in an energy, sustainability, natural resources, M&A, technology, industrials or other relevant sector; (b) project development, M&A or finance in a large IPP, utility or energy company; or (c) investment analysis for a buy-side energy investor. For more information, click here.

Impact Secondaries

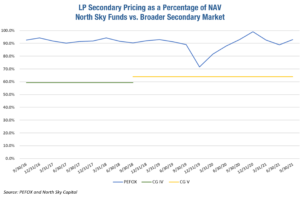

Pricing Comparison. Pricing in the broader secondary market has been somewhat volatile since March 2020 (covid). As shown in the chart below, pricing dropped precipitously as covid set in and then began a sharp recovery. Pricing then overshot the long-term average at yearend 2020 and has since returned to normal levels during Q1-3 of 2021.

Hidden within these composite numbers is the pricing within the various subsectors. Megabuyout funds tend to price roughly at or slightly below NAV, other buyout funds (assuming they are mature portfolios) price just below that (e.g., 90-95% of NAV). Next in the pecking order are growth equity/late-stage venture funds (again assuming mature portfolios) typically price around 85% of NAV and below that are the early-stage venture funds at 80% of NAV. Weighting in terms of size and volume follows the same order with more buyout funds trading hands than venture funds, resulting in the composite curve you see below.

We have added the average purchase price for our impact secondaries funds onto this chart to show that impact secondaries are pricing even more favorably for the buyer than the broader marketplace. The impact secondaries market is still nascent and less competitive. We have been taking advantage of this since 2013 when we launched the first impact secondaries fund in the world (Clean Growth III). Pricing for CG IV and V overlap with the data on the chart below and demonstrate our pricing power in this inefficient niche (or specialty) marketplace. CG IV’s average LP secondary pricing was 59% of NAV and CG V’s pricing was 63%. We have very little direct competition still and investors with us understand the reasons (knowledge, relationships with GPs, proactive sourcing and deal size).

Of course, LP secondaries are just one of the three ways we are investing, with preferred equity and continuation vehicles being the other two structures used. During the depths of covid, the bid ask pricing for impact secondaries was too large to transact, so we pivoted to preferred equity and continuation vehicles at that time. All three tools are important and their usage varies as the market flows through its ups and downs.

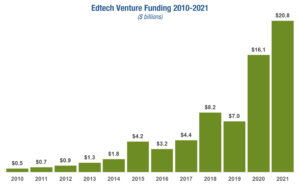

Uptick in Edtech Investments. We are seeing a strong flow of capital into edtech companies—see chart below. Part of that is a driven by covid and the movement toward remote learning for kids and college students, as well as the rather new continuous learning movement embraced by the Gen X and Baby Boomer generations. But the movement is truly global as students in India, Africa and elsewhere also come online and take advantage of these new learning channels to improve their station in life. Venture capitalists and others are ploughing new money into edtech as a result. Per our friends at GSV Ventures, “[Edtech] attracted record levels of venture investment ($20+B in 2021) but also record levels of M&A activity (also $20+B) alongside an active IPO market.” Numerous edtech-focused funds have been raised recently from first-time fund managers as well as experienced managers like GSV Ventures, Reach Capital and Learn Capital. North Sky’s impact secondaries funds have made initial investments in edtech portfolios, and we expect to increase our investments here in the near term.

How Do We Deliver Impact Through Secondaries? As a secondary investor, we are sometimes asked this question. The question is usually framed this way: “If you are merely buying someone else’s interest in an already existing impact fund or ESG focused company, how does that create new impact? Or to use an analogy, if you are trying to spur automobile production, buying a used car does no good, right?” The problem with this framing is that it does not align with what we really do.

We deliver impact to our LPs in two ways: (a) buying LP interests in existing funds and (b) investing additional capital in preferred equity or continuation vehicles. Let’s take each in turn.

When buying LP interests, impact is created in two ways. First, there often is additional capital to be called after we purchase the interest, so new capital is flowing into these portfolios and we are creating “new” impact. Second, institutional investors now know there is a secondary market for impact investments, which allows previously hesitant impact investors to dip their toe in the water. If they change their mind down the road, there is an exit path for them. This has helped to expand the number of impact investors and the dollars flowing into venture capital, growth equity, buyout and infrastructure funds across the board. Our funds are creating a deeper and more liquid impact marketplace and performing a market clearing function that is necessary for a healthy and growing marketplace. For context, buying LP interests represented about 50% of the investments made in Clean Growth V (as of 9/30/21).

When making preferred equity investments, we are always creating new impact as our capital is being used as growth capital for one or more companies. So the impact we are creating here is obvious. Similarly, when making continuation investments, we almost always are providing a liquidity solution to some of the previous investors while also providing fresh growth capital for the portfolio (one or more companies). Again, whenever we are injecting growth capital, we are spurring new impact. Preferred equity investments and continuation investments each represented about 25% of the investments made in Clean Growth V (i.e., together they made up about 50% of the investments in that fund).

Conclusion

The world is transitioning to a cleaner, sustainable energy future. North Sky is playing a central role in that transition. Our two flagship strategies are well-suited and well-positioned for today’s volatile environment.