Introduction

Rampant inflation, rising interest rates, the bear market for stocks and other political and economic factors are causing investors to rethink how and where they want to invest. Some are also using this moment to tilt their portfolios further into ESG and impact investments.

Today there are more Impact/ESG choices than ever, especially in private markets. The options are vast: big/small, global/regional, broad/specialty, attractive returns/concessionary, environmental/social, venture, buyout, infrastructure, real assets, etc. It is a much bigger tent today than when we started fundraising for our first impact fund in 2005. We welcome everyone to the party.

We are very enthusiastic about our corner of the marketplace, too—sustainable infrastructure and impact secondaries (private equity). We believe we are riding a multi-decade investment opportunity as the world shifts to more sustainable practices in areas like energy, transportation, food, water, sanitation and healthcare. A confluence of recent events is accelerating this transition, including inflation (specifically the doubling of gas and diesel prices since January 2021) and the steady 15-year-long decline in the costs of renewable energy, energy storage (batteries), water treatment, indoor agriculture and other sustainable technologies.

Inflation

Our goal here is to explain how technological advancements, economic factors and policy shape the impact/ESG landscape generally and our investment strategies specifically. We acknowledge the negative headlines of the last several months but find cause for optimism among it all. Disruptive forces create opportunities for passionate, experienced and nimble investors!

Market Update

Market conditions. In volatile times like these, our impact secondaries strategy takes on a tinge of special situations or even distressed coloring. Our knowledge, experience and flexibility enables us to unlock value in our little section of the private equity marketplace. Just as we enjoyed buying opportunities in early 2020 due to the onset of covid, recent market volatility seems to again be favoring buyers like us who offer flexible structuring solutions to both private equity funds and limited partners in those funds. In the last 90 days, our focus has pivoted from traditional LP secondary purchases to preferred equity (structured) transactions. The main reason is that the reporting lag of private equity funds has created a widening of the bid-ask spread. LPs still think their LP interest should be valued at the level reported to them as of yearend, while buyers today know the transaction prices should be generally lower due to subsequent pricing signals in the stock market, inflation and macroeconomic factors. In many cases right now, there is too big a gap between the bid and ask prices for traditional LP secondaries, so few of those types of deals will happen until that gap shrinks. However, a preferred equity solution effectively bridges that gap in many cases because buyer and seller don’t have to agree on the value of the asset today, but rather only how they will distribute future proceeds as the portfolio is liquidated in the future.

GP-led opportunities have also hit a speed bump. GP-led deals have been the darling of the secondary market for last 4-5 quarters but recently we have seen a longer time to close, price reductions and even some deals being scrapped altogether. Today’s successful transactions tend to have companies that are exceeding their budgets year-to-date AND prices that have been reduced from the initial indicative offers. Like most years in the secondary market, 2022 is setting up to be heavily backend weighted from a volume perspective.

Update on CG VI. We have made our first investment from the new fund, Clean Growth VI, and it was indeed a preferred equity transaction with a fund managed by a GP we have known for nearly 20 years. As a brief reminder, our highly differentiated secondaries strategy is focused primarily on buyout, growth equity and venture capital opportunities across climatech, sustainable food, circular economy and healthy living.

Since we created the impact secondaries marketplace in 2013, we have seen an increase in deal flow each year. The growth in the last 18 months has been phenomenal. As the average size and number of impact funds offered to investors has increased in recent years, so too has the number and size of impact secondary opportunities for us. With a near-term opportunity set that exceeds $500 million, we are just reaching the tip of the iceberg in this specialty secondaries market. We are very bullish about putting new capital to work in the foregoing sectors and in this environment today.

On the other hand, we believe exits for some of our existing holdings in prior funds will be pushed out by perhaps a quarter or two. 2021 was a very strong year in terms of both M&A and IPO exits. M&A activity is still continuing but IPOs have slowed considerably for the moment.

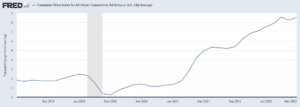

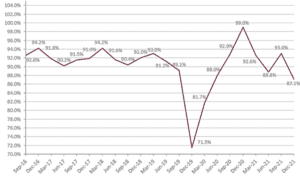

Secondary pricing. Pricing fell to an average of 87.1% for the broader secondaries market (prices based on 12/31/21 NAV). As noted above, a lot of this is due to negative economic events post-yearend and the big gap between sellers’ hopes and the reality of what buyers are willing to pay today. According to PEFOX, many of the biggest secondary buyers have pulled back, expecting there will be bigger discounts soon, and thus transaction volume has dropped significantly. There seems to still be a fair amount of activity for smaller pieces of the big brand name funds. Smaller players who choose to stay active seemingly have less competition and may be able to find bargains. That said, we believe the best way to transact in this market is not so much through purchasing LP secondaries outright, but rather through preferred equity transactions that are structured to meet or exceed our returns hurdles while securing better downside protection.

Average Secondary Pricing

Inflation’s affect on sustainable infrastructure. Investors are generally recalibrating their portfolios and seeking investments that can withstand today’s high inflation rate (8.6%). Investing in the stocks of companies with pricing power or in other situations where revenue rises with inflation seems top of mind. Popular “safe haven” stocks being touted on the financial news channels are Exxon, Altria and Newmont Mining but those come with obvious negatives from an ESG/Impact standpoint. We believe our sustainable infrastructure strategy offers a better alternative. Not only are we financing and building the renewable energy infrastructure needed for a sustainable tomorrow, but many of our projects have inflation adjustment features built into their offtake agreements. That means whether we are selling renewable natural gas (RNG) made from organic waste or electricity from a solar or hydro project, the price can rise as inflation rises. Sometimes sales prices are tied directly to CPI. In other cases it may be tied to local or regional electricity prices, so as those prices rise the revenue from our projects rise, too.

Higher costs are another matter, whether that is for construction labor, raw materials or equipment. For a typical North Sky project, the financing and construction window is quite short compared to much of the infrastructure market. For example, we might build a 5 MW community solar project that takes six months to construct and energize, or we might take twelve months to retrofit a food waste site to turn that waste into RNG and fertilizer. These are relatively short periods and costs are negotiated prior to us putting any significant capital at risk. Contrast what we do with constructing a large combustion power plant or a new toll road. Those big projects might stretch out over multiple years. The shorter the project time, the less chance there is that labor and other costs will accumulate into large cost overruns and impair the investment.

Higher interest rates’ affect on sustainable infrastructure. In areas like utility scale solar and wind, where profit margins are already thin, any meaningful increase in debt costs for that project can have a material adverse effect. We expect IRRs for big wind and solar projects to decline. The impact of higher rates should be more muted for higher profit margin infrastructure projects like RNG, waste-to-value and specialty areas such as community solar, energy storage and EV charging (at least in some regions).

Update on solar tariff issue. On February 8, 2022, a small US-based solar panel manufacturer named Auxin Solar Inc. requested that the Department of Commerce initiate inquiries into whether solar cells and modules assembled in Cambodia, Malaysia, Thailand or Vietnam, using parts and components from China, were circumventing the “antidumping” rules. The Department of Commerce began an inquiry on March 25, 2022, and it is still ongoing. If there has been a violation, up to a 250% tariff could be applied to panels purchased from those countries. The potential risk of huge tariffs being imposed ex post facto effectively put US solar projects on hold if they included panels from those countries. The matter has been at least temporarily resolved in favor of the solar industry. On June 5, the White House announced a 24-month tariff exemption on solar modules manufactured in Cambodia, Malaysia, Thailand and Vietnam.

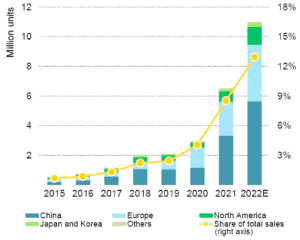

Inflection Point in Electric Vehicle Sales. We thought the chart below was interesting and illustrative of the transition away from fossil fuels and toward renewables. EV sales doubled from 2020 to 2021, with a record 6.6 million EVs sold worldwide last year. EV sales represented nearly 10% of all global car sales in 2021 and sales are expected to grow to represent 16-17% of global sales in 2022. Two million EVs were sold in the first quarter of this year. China and Europe sales represent the largest shares, but the USA is coming on strong as the number of EV models to choose from has increased, broadening EV appeal here.

Global EV Sales and Market Share

As EV sales continue to grow, we see the need for more support infrastructure, including more EV charging stations, energy storage systems, grid stabilization technology and of course more renewable energy generation.

New solar PV record efficiency. Technological progress marches on! In mid-May, the latest solar cell from NREL set a world-record for efficiency of 39.5%, using quantum wells and a triple-junction design. The quantum wells precisely tune three light absorbing layers to convert photons into electrons from different parts of the light spectrum. The design is also relatively simple (and likely less costly to mass produce) compared to other recent record-breaking solar cell designs.

Update on infrastructure funds I and II: 2021 was a terrific year for our prior sustainable infrastructure funds as we exited three investments from our second fund and positioned the handful of remaining investment in our first and second funds for a similarly successful 2022. The average gross IRR from these three investments was 17.7%. We are working on several more exits and expect to sell three additional investments in Fund II soon and one of the two remaining investments in Fund I.

Update on infrastructure fund III: Fund III, which we refer to as “IIF,” should be fully committed in the coming weeks. We’re pleased to report the Q2 closing of a 200 MWh battery storage investment we had previewed in our Q1 commentary. In this case, we partnered with an experienced developer with attractive projects in the NYC metro area. We believe in the long term need for electricity storage in this region due to transmission congestion and look forward to funding the developer’s future growth.

Update on infrastructure fund IV: Fund IV, which we refer to as “SIF IV,” has several investment opportunities under review. We expect to make the first investment in the near future.

Conclusion

We are playing an active role in the global transition to a more sustainable future. That transition appears to be a multi-decade investment opportunity in major areas like energy, transportation, food, water, sanitation and healthcare. Our flagship strategies are differentiated, authentic and impactful. We hope you will join us if you haven’t already. To learn more, please contact Gretchen Postula.

We also wish our American readers a happy Independence Day and a safe holiday weekend!