Introduction

Wow, what a year this has been! We are incredibly grateful to the new people and institutions that have joined forces with us to use investment capital to make the world a better place. As we bring this year to a close, we thank our incredible community of investors, consultants, service providers, friends and family who have helped make this such a successful year in terms of investment returns, liquidity events, impactful investment outcomes and overall growth at North Sky.

While we recognize the difficult investment and macroeconomic conditions that exist today in the public markets, we have never been more optimistic about our near-term prospects for making great investments on behalf of our LPs. For those of us lucky enough to be tasked with investing in impact/ESG sectors, opportunities are abundant, allowing us to be very selective. For example, return profiles for certain renewable natural gas, community solar and energy storage are penciling to 200-500 bps higher than this time last year.

We are growing too. This year, we made our first investments for Clean Growth Fund VI (impact secondaries) and lined up our first investment for Sustainable Infrastructure Fund IV (Sustainable Infrastructure). We also launched Paddle Energy to pursue the enormous opportunity available today in community solar development. Paddle recently closed its first investment, a 1.5 MW community solar project in Maine.

In addition, we hired Erika Gucfa (July) and Anthony Doan (November) and are hiring for one Analyst position on the secondaries team and one Associate position on the infrastructure team—see current job postings here. We expect to hire two or three more people in the second half of 2023. Finally, we are opening an office in Europe in January, which will be led by a senior investment professional whom we have known for more than 15 years and whom we consider to be one of the most experienced and knowledgeable impact fund investors in Europe. We are very excited about this addition, and there will be a formal announcement in the next few weeks.

If you are interested in learning more about our investments, please contact Gretchen Postula or Erika Gucfa.

US SIF Biennial Report

US SIF just released the 14th edition of it Report on US Sustainable Investing Trends. North Sky Capital is proud to be a lead sponsor of this report. The report shows that, as of the beginning of 2022, there was $8.4 trillion invested in US sustainable investments, which represents 13% of all US assets under professional management. To access a complimentary copy of the executive summary, click here.

Market Update

We are continuing to see very attractive investment opportunities in our areas of focus, including renewable natural gas, community solar and energy storage. All these areas and other sectors have been buoyed by the Inflation Reduction Act. Community solar has also been incentivized further by policy support in specific states, such as Illinois, Maine, Minnesota and New York. To take advantage of the vast array of opportunities in community solar and as noted in the introduction above, we launched Paddle Energy. Paddle Energy is led by Operating Partner Dale Freudenberger, who previously founded FLS Energy, a very successful solar developer in the mid-Atlantic region and one of North Sky’s best infrastructure investments ever. Dale is supported by Pat Kay and others who have significant solar development expertise. Paddle has entered into a Development Services Agreement to invest in community solar projects on behalf of our third infrastructure fund. We expect Paddle will eventually agree to a similar arrangement for the benefit of SIF IV.

Sustainable infrastructure investing has grown substantially in popularity among institutional investors over the last few years and for good reason! The global transition away from fossil fuels and toward renewables is now a formidable, long-term trend that offers attractive investment returns for experienced GPs and developers.

Among the key issues we are following here at North Sky are prices of solar PV modules and batteries. There has been a general increase in prices of both modules and batteries over the last year or so. Availability also has been spotty for both products lately. The reasons for the spottiness for modules are tariffs and supply chain issues, mostly relating to plant shutdowns due to China’s zero covid policy. The reasons for batteries are lingering supply chain problems and demand has been outstripping supply in recent months.

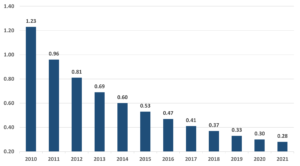

For many years, solar module prices, measured at the factory, have exhibited a steady decline due to economies of scale. In the illustrative chart below, the price of Chinese modules has decreased from $1.23 per watt in 2010 to just $0.25 per watt today. This of course is prior to any shipping costs or tariffs, which are generally higher today than in 2010.

Chinese c-Si Module Prices (BNEF)

Source: Bloomberg New Energy Finance

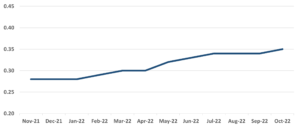

Despite this long-term trend, prices for modules installed in the USA and Europe have increased substantially this year. As you can see in the chart below, the wholesale price for mainstream modules was about $0.28 per watt in November of 2021 but rose to about $0.35 per watt by November 2022. That is a 25% increase over the last year. “Mainstream” modules mean modules made from poly- or monocrystalline cells, which are used in commercial PV systems and have an efficiency of up to 21%.

Mainstream Solar PV Panel Prices (Wholesale $/W)

Source: pvxchange.com

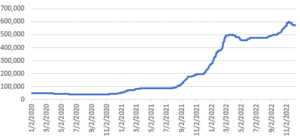

The supply-demand imbalance for batteries mentioned above drove prices much higher. To illustrate this we can look at the rapid rise in price of one of the main components of batteries, lithium carbonate.

Lithium Carbonate Pricing – 99.5% Battery Grade (RMB)

Source: Bloomberg

What stands out to us is that in just this year, from January to November, the price went from ¥277,500 to ¥577,500, a 108% increase. It seems demand is rising and supply is not quite keeping up. The additional increase at the far right of the chart is due to the market’s reaction to the passage of the Inflation Reduction Act, which further increased demand and pushed prices up another 20% from August 16, 2022 to November 30, 2022. While prices have leveled off, battery storage projects will require premium revenues to compensate for these elevated costs.

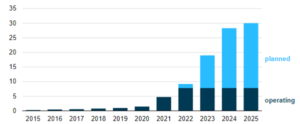

In spite of record high prices, installations of batteries worldwide are still expected to markedly increase. Here in the USA, there was almost a negligible amount of energy storage prior to 2021. Energy storage developers have been busy the last two years and are now planning to more than triple the installed base of energy storage systems over the next three years from roughly 9 GW today to 30 GW by the end of 2025 (see chart below).

U.S. Battery Storage Capacity (2015-2025) gigawatts

Source: US Energy Information Administration, Battery Storage Capacity Forecast

The US energy storage market is one of three key areas we are focusing on with SIF IV and one where we see vast opportunity over the next few years.

There are two important undercurrents happening right now that we are using to our advantage.

- This is a very complicated environment for all investors and seemingly the most difficult to navigate since the great financial crisis. It stems from a combination of inflation, higher interest rates, earnings slowdown, recession fears, supply chain problems, labor shortages and other factors. These are nerve-wracking conditions whether you are the CIO of a family office or pension plan, the manager of a hedge fund or a GP of a VC or LBO fund. It comes as no surprise that recent new deal activity has slowed. Using venture capital data from Pitchbook as a barometer, we see that new investment activity in Q3 was at the lowest point in nine quarters, indicating concern about global economic conditions. However, there are important exceptions. New deal activity across many of the areas we focus on—cleantech, healthcare, energy and transportation—have remained quite strong. During just the first three quarters of this year, activity in those sectors were essentially equal or greater than the activity for all four quarters in 2020. Furthermore, venture investment in “clean energy” companies is on pace this year to equal the $15B high point for such investments set last year.

- Exit activity plunged in 2022. It appears 2022 will be the worst year for IPOs since 1990. IPO data from Refinitiv shows only 74 companies went public in the USA, raising a total of just $8 billion so far this year, with virtually nothing left on the upcoming calendar. Further, IPO proceeds were down a stunning 95% from 2021, and at least 50% lower than any of the past 31 years. The number of IPOs was also down 88% compared to last year, coming in at the lowest level since 2009. Per Pitchbook, Global M&A deal activity also declined in Q3, the third such quarterly decline in a row. M&A exits likely will come in lower than last year but above pre-pandemic levels. In sum, exit activity has clearly slowed this year.

So what does that mean for us as impact secondaries investors?

- The areas we cover are still going strong in terms of new deal activity, thanks in part to investor appetite for impact/ESG areas, the Inflation Reduction Act and various state level policies and incentives for things like energy storage, EV charging, waste management, renewable energy generation, grid stabilization and local job creation. The incentive for onshoring manufacturing of things like solar cells and batteries is also driving new investment opportunities for us.

- A slowdown in exits and an increase in economic uncertainty tend to drive new secondary investment opportunities as GPs and LPs react to the changes, whether that be in the form of traditional LP secondaries, continuation vehicles or preferred equity (structured) deals. We have already closed three secondary investments for CG VI and approved two more that are in a closing process. Other investments are lining up for Q1. We expect the closed investments as of yearend to be valued at approximately 1.8x cost. Furthermore, we expect 2023 to be a huge year for secondaries investors broadly and North Sky in particular. The combination of a denominator effect and a slowdown in exits means many institutional investors are likely sellers of private equity interests next year, setting us up potentially for a buyer’s market.

- In the very near-term, our preference is for traditional secondaries with good portfolio diversification and preferred equity transactions that help us bridge the gap between the price we are willing to pay and that which the seller is willing to take. That pricing gap has been increasing throughout the year but we expect it to begin to narrow when the yearend valuations begin to be posted (i.e., when the auditors begin to nudge GPs to decrease valuations to reflects the macroeconomic backdrop). We are focused on high quality assets in non-cyclical industries like sustainable food/agriculture and healthcare. We are still seeing interesting GP-led opportunities, but our strong preference is for multi-asset portfolios rather than single-asset (rifleshot) opportunities. There would have to be very compelling reasons for us to do a single asset continuation vehicle at the moment.

Admittedly, the slowdown in exit activities does have a near-term negative effect on our existing investments in CG III-V. That said, we continued to see positive development across the Clean Growth portfolio during Q4. On the liquidity front, financial and strategic buyers remained broadly interested in impact companies given the strong financial and social tailwinds. Notably, Breezometer was acquired by Google for over $200 million and EnOcean agreed to merge with a special purpose acquisition company at an equity value of $120 million. Portfolio drivers also continued to raise new funding, with ZincFive closing a $54 million round and Minesense raising $42 million. Both were “uprounds,” meaning valuations increased. Finally, on December 13, scientists at the Lawrence Livermore National Laboratory in California announced they achieved a breakthrough with respect to nuclear fusion when the energy output from their device was greater than the energy input. CG IV and V have investments in one of the most promising fusion companies, General Fusion. The latest news shows we are one step closer to a nuclear-powered future, without long-lived radioactive waste.

Conclusion

We feel blessed to have been doing work we love for nearly 24 years. We are grateful to the many investors who have joined us across all our funds. With stock and bond market volatility, inflation and macroeconomic uncertainty, many investors are looking to us to deliver attractive returns and stability. We are here to guide you through the storm. With the Q3 passage of the “green new deal” and the secular trends of increasing demands for cleaner, greener ways of doing everything from manufacturing, farming, waste treatment, water purification, energy production and transportation to simply wanting to live healthier, more sustainable lives, we have never felt the wind at our back as much as we do right now. We are excited to keep applying our experience and insights to the opportunities that lay ahead.

We wish you a happy Hanukkah, a very merry Christmas and a prosperous and healthy New Year!